As digital finance continues to expand, Gate Card and Traditional Visa Debit Card represent different approaches to storing and transferring value. One is built on blockchain-based assets and exchange mechanisms, while the other relies on long-established banking networks and payment rails. This contrast reflects broader changes in how users access liquidity, manage assets, and interact with global payment systems.

Overview of Gate Card and Traditional Visa Debit Card

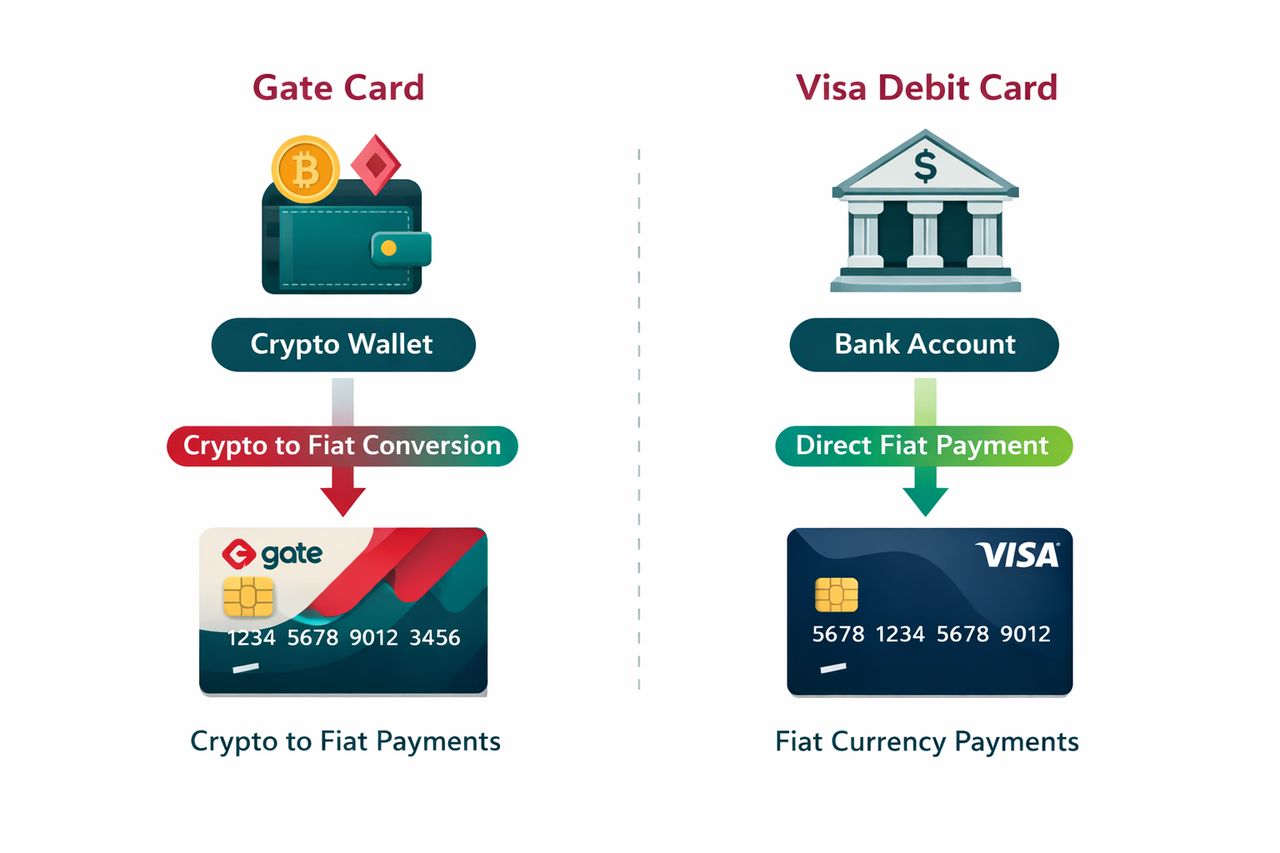

Gate Card and Visa debit cards represent two distinct yet increasingly interconnected payment frameworks.

Gate Card acts as a digital asset credit card issued by Gate that enables eligible users to spend or withdraw funds using cryptocurrencies across supported payment scenarios. It is designed for use in online transactions, in-store purchases, ATM withdrawals, and other payment environments.

Traditional Visa debit card is issued by a financial institution and linked directly to a bank account. Payments are processed by deducting fiat funds immediately, using established clearing and settlement systems.

The key distinction lies in the underlying asset layer and infrastructure: crypto-based conversion versus direct fiat settlement.

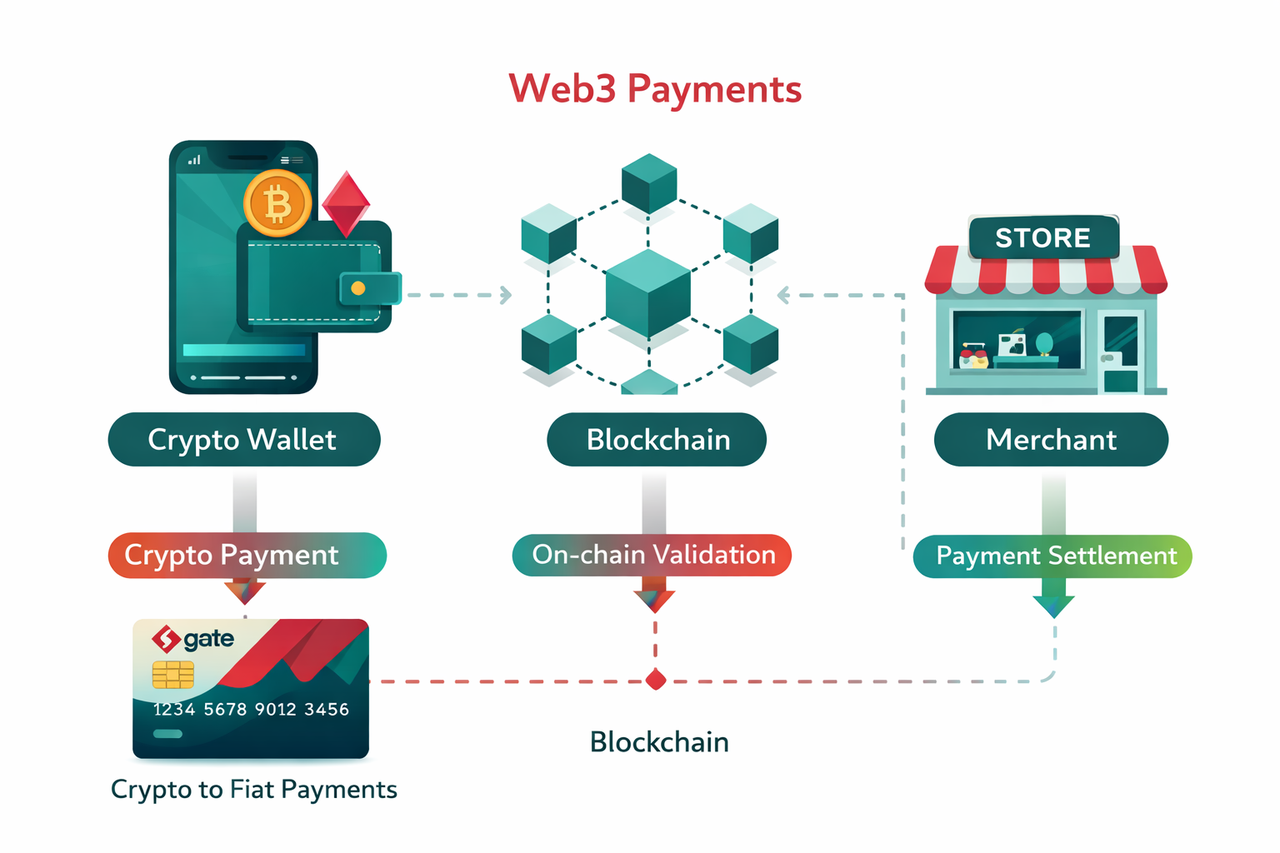

The Advantages and Differences of Web3 Payments

Web3 payment systems introduce a structural shift in how transactions are initiated, processed, and settled.

-

Decentralized asset ownership:Users retain control of their assets through cryptographic wallets rather than relying entirely on custodial banking systems.

-

Borderless transaction capability:Crypto-based payments can operate across jurisdictions with fewer intermediaries, reducing reliance on regional banking networks.

-

Programmable financial logic:Smart contracts enable conditional payments, automated settlements, and integration with decentralized applications.

-

On-demand liquidity conversion:Crypto cards convert assets in real time during transactions, reducing the need for manual exchange steps.

These characteristics position Web3 payments as flexible alternatives within a broader financial ecosystem dominated by centralized systems.

Core Differences Between Gate Card and Visa Debit Cards

The differences between the two systems can be summarized across key structural dimensions:

| Dimension |

Gate Card |

Traditional Visa Debit Card |

| Underlying Asset |

Cryptocurrency (BTC, ETH, stablecoins) |

Fiat currency (USD, EUR, etc.) |

| Account Type |

Crypto wallet / exchange account |

Bank account |

| Transaction Process |

Real-time crypto-to-fiat conversion |

Direct fiat deduction |

| Infrastructure |

Blockchain + exchange systems |

Banking + card networks |

| Settlement Logic |

Conversion-based settlement |

Immediate fiat settlement |

These differences influence transaction predictability, system dependency, and user control over assets.

Fee Comparison Between Gate Card and Visa Debit Cards

Fee structures differ due to the operational mechanisms behind each system.

| Fee Type |

Gate Card |

Visa Debit Card |

| Transaction Fee |

Conversion spread may apply |

Usually none for domestic payments |

| Foreign Transaction |

Based on crypto conversion rates |

Typically 1–3% fee |

| ATM Withdrawal |

May include service + conversion cost |

Fixed or network-based fee |

| Maintenance Fee |

Depends on provider |

Bank-dependent monthly fee |

| Network Cost |

Blockchain fees (variable) |

Not applicable |

Gate Card fees are often variable due to market conditions and network activity, while debit card fees are generally more standardized and predictable.

Cashback Mechanism Comparison Between Gate Card and Visa Debit Cards

Cashback systems reflect fundamentally different reward structures tied to asset types.

| Feature |

Gate Card Cashback |

Visa Debit Card Cashback |

| Reward Type |

Cryptocurrency or platform tokens (e.g., BTC, ETH, USDT, GT) |

Fiat currency |

| Distribution Logic |

Tier-based system; higher tiers can unlock up to 5% cashback |

Fixed percentage based on spending |

| Fee Structure Impact |

~1% card fee, which can be offset or exceeded by rewards at higher tiers |

Typically no direct fee-reward linkage |

| Value Stability |

Fluctuates with market price changes |

Stable and predictable |

| Financial Behavior |

Rewards may increase or decrease in value over time |

Maintains consistent purchasing power |

Gate Card uses a T0–T4 tiered framework where cashback rates and monthly reward caps increase at user level. Higher-tier users can access up to 5% cashback, with a progression-based structure designed to encourage sustained usage and asset participation.

Usage Scenario Comparison Between Gate Card and Visa Debit Cards

Gate Card usage scenarios:

Spending crypto holdings without manual conversion allows users to pay directly with their cryptocurrency balances, as the system automatically converts assets into fiat at the point of transaction. This simplifies the payment process and removes the need for separate exchange steps.

Cross-border payments without relying on traditional banking systems make Gate Card suitable for international use, especially in situations where banking access is limited or inefficient. Digital assets can be transferred and spent globally with fewer intermediaries.

Accessing liquidity from digital assets enables users to treat their crypto holdings as a readily available source of funds. Instead of converting assets in advance, they can use them dynamically when making purchases.

Visa debit card usage scenarios:

Daily purchases such as groceries and transportation are the primary use cases for Visa debit cards, as they are widely accepted and directly linked to bank account balances.

ATM withdrawals and salary-linked spending allow users to access cash and manage income deposited into their accounts, making debit cards central to routine financial activity.

Integration with traditional financial services ensures compatibility with bill payments, subscriptions, and payroll systems, reinforcing the role of debit cards within established banking infrastructure.

Gate Card is often aligned with digital asset ecosystems, while Visa debit cards remain central to routine economic activity.

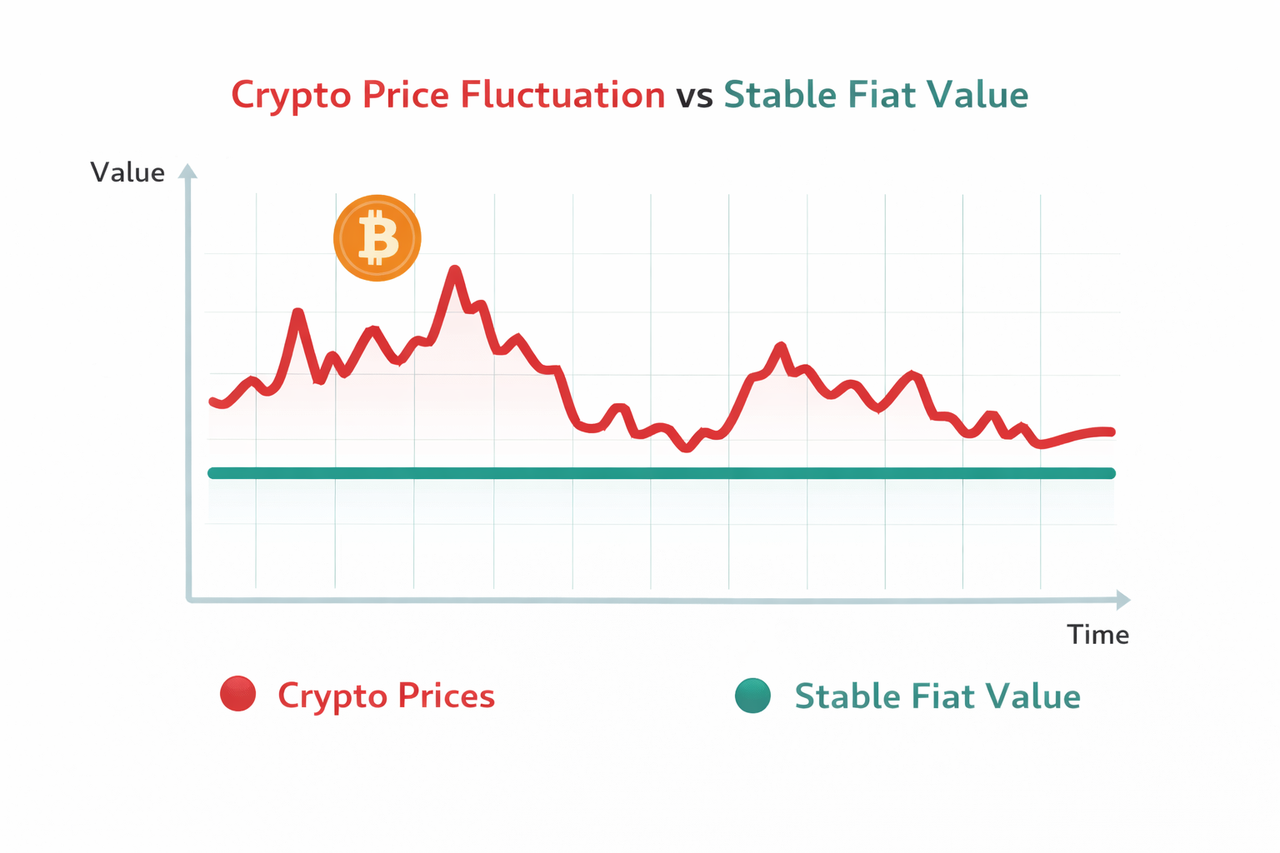

Comparison of Asset Types and Volatility Between Gate Card and Visa Debit Cards

Gate Card assets:

-

Primarily use cryptocurrencies, including both stablecoins and volatile digital assets

-

Subject to market-driven price movements, with values that can change significantly in short periods

-

Purchasing power may fluctuate between holding and spending

-

Require timing considerations when used for payments

Visa debit card assets:

-

Use fiat currencies issued and regulated by central banks

-

Maintain relatively stable value in the short term due to monetary policy

-

Provide consistent and predictable purchasing power

-

Support straightforward spending without timing concerns

This difference directly affects how users approach budgeting, financial planning, and spending behavior, with crypto-based systems requiring more awareness of price fluctuations compared to fiat-based systems.

Risk and Stability Comparison Between Gate Card and Visa Debit Cards

Risk profiles differ because each system is built on a different financial foundation. Gate Card operates within the crypto ecosystem, where value and infrastructure can be more dynamic, while Visa debit cards rely on established banking systems that prioritize consistency.

Gate Card risks: Gate Card is exposed to crypto market volatility, meaning the value of assets used for spending can change quickly and affect purchasing power. It also depends on exchange infrastructure and liquidity, so transaction efficiency may be influenced by market conditions or technical factors. In addition, regulatory uncertainty across jurisdictions can impact how crypto-linked payment services operate

Visa debit card risks: Visa debit cards are generally stable for everyday use but rely on centralized financial institutions. This introduces the possibility of account restrictions or controls imposed by banks. They are also subject to fraud and unauthorized transaction risks, although protections are typically in place. Their reliability depends on the stability of banking systems and payment networks.

Each system reflects a trade-off between flexibility and predictability, with Gate Card offering greater exposure to digital assets and Visa debit cards providing more consistent day-to-day stability.

Conclusion

Gate Card and traditional Visa debit cards illustrate two parallel approaches to modern payments. One integrates blockchain-based assets into real-world spending through dynamic conversion, while the other operates within established banking frameworks using stable fiat currency.

Their differences in fees, cashback structures, asset behavior, and risk profiles reflect broader shifts in financial infrastructure. Understanding these systems helps clarify how users navigate both traditional and emerging payment environments based on their financial needs and asset preferences.

FAQs

1. What is the main difference between Gate Card and Visa debit cards?

Gate Card enables spending of cryptocurrency through real-time conversion, while Visa debit cards use fiat funds directly from bank accounts.

2. Are Gate Card fees fixed?

No, they can vary depending on market conditions, conversion rates, and blockchain network activity.

3. Which cashback system is more stable?

Visa debit card cashback is more stable because it is denominated in fiat currency.

4. Can Gate Card be used for everyday purchases?

Yes, provided the payment network supports the transaction and conversion is available.

5. Do both cards support international payments?

Yes, but they differ in how currency conversion and fees are applied.