Bitcoin enters the weekend trading around $72,000, significantly lower than last week’s peak of over $74,000 and still far from the highs reached earlier this year. Looking solely at price movements, the market appears relatively stable.

However, the underlying structure suggests a much less solid picture.

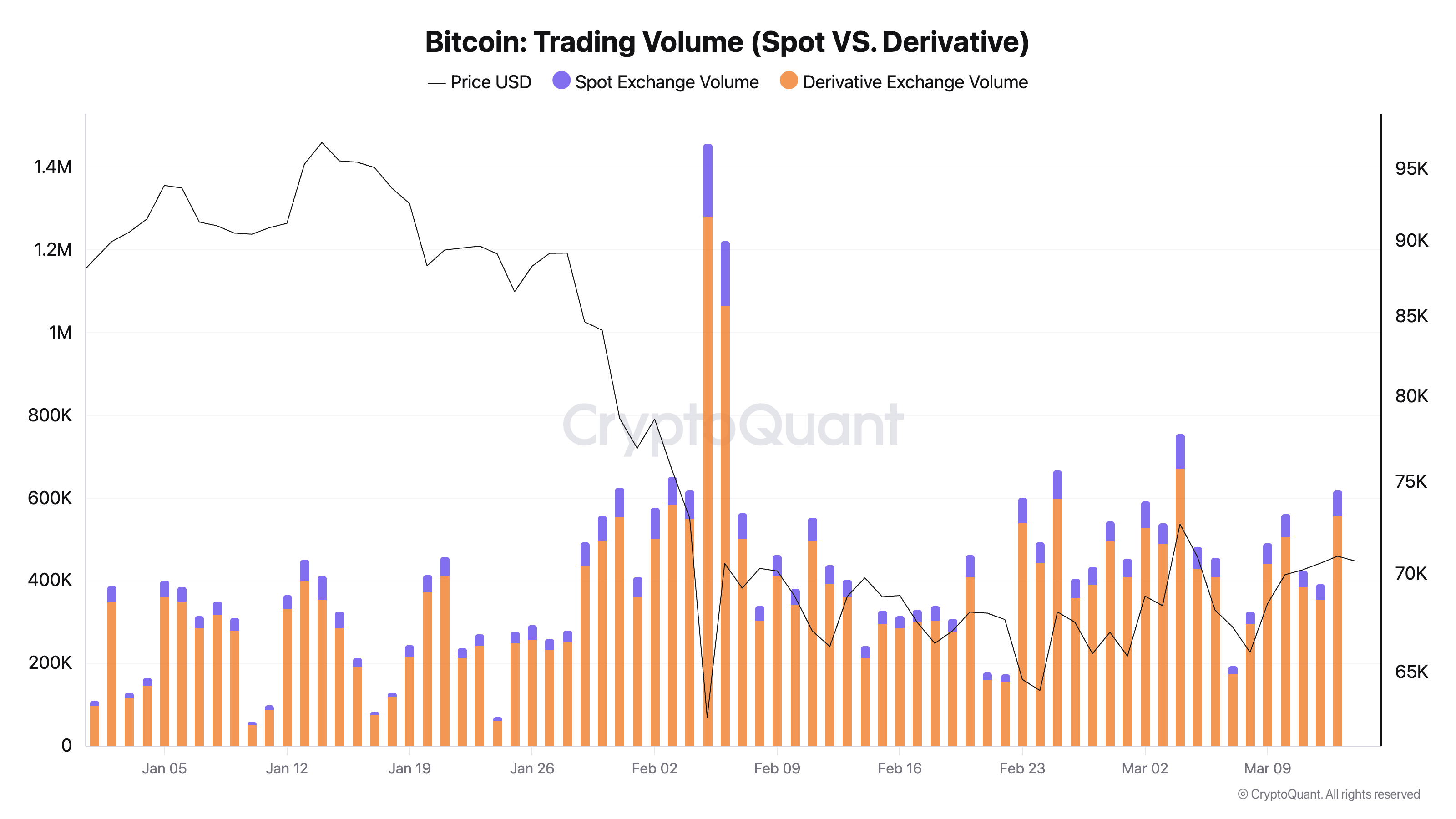

Data shows that spot trading activity is weakening, while derivatives are increasingly taking a dominant role. Nearly every day this month, derivatives trading volume is about nine times higher than spot — a sign that market momentum isn’t driven by genuine demand to buy Bitcoin. Instead, the market is primarily supported by leverage.

Chart showing total trading volume of Bitcoin spot and derivatives on exchanges from January 1 to March 13, 2026 (Source: CryptoQuant)## The Difference Between Spot and Derivatives Markets

Chart showing total trading volume of Bitcoin spot and derivatives on exchanges from January 1 to March 13, 2026 (Source: CryptoQuant)## The Difference Between Spot and Derivatives Markets

Spot trading means investors buy BTC directly from the market and actually own the coins. This reflects demand very clearly: if many people are willing to buy and hold Bitcoin, prices will rise. Conversely, if demand is weak, sellers must lower prices to find buyers, pushing the market value down.

Meanwhile, derivatives are more complex financial instruments that allow traders to implement various strategies through futures, options, basis trading, or short-term hedging, often with leverage.

These strategies help maintain liquidity and price volatility but also make the market appear “deeper” than it actually is. When most activity is in derivatives, prices become heavily dependent on trading positions and can experience sharp drops when positions are liquidated.

Growth in Contract-Based Rally Rather Than Genuine Demand

Total trading volume of spot and derivatives on centralized exchanges decreased by about 2.4%, down to $5.61 trillion in February — the lowest since October 2024.

This decline mainly stems from spot markets, while most trading activity remains concentrated in derivatives.

Global spot trading volume has fallen significantly, while synthetic exposure via derivatives continues to increase. This is very different from sustainable rallies driven by expanding spot demand.

Last week’s Bitcoin price movement is a prime example. BTC recovered above $70,000, seemingly indicating renewed buying interest. However, most of this rebound came from leveraged activity rather than genuine spot buying.

This doesn’t mean futures or options volumes are negative. The Bitcoin market has evolved to the point where derivatives play a crucial role in price formation. Still, when prices stabilize amid weak spot demand, the upward momentum can be much more fragile than it appears.

The reason is that support from trading positions can be closed very quickly, rather than from real investors buying and holding Bitcoin.

Increasing Role of Institutions

The deeper involvement of financial institutions means this trend is no longer just a crypto market internal issue.

In early February, CME announced their crypto products recorded record trading volumes in 2026, with daily crypto derivatives volume up 46% year-over-year. This indicates institutional exposure to Bitcoin continues to grow strongly, mostly through managed derivatives.

Using futures contracts doesn’t necessarily reflect weak confidence in Bitcoin. Often, large institutions use these tools to access markets and hedge risks efficiently.

However, the impact on the market remains the same: Bitcoin’s daily price behavior is increasingly shaped by financial contracts rather than direct asset purchases.

Risks in a Worsening Macroeconomic Environment

This shift wouldn’t be too concerning in a stable macro environment. But Bitcoin is currently trading amid rising global risks.

On March 13, US equity funds experienced their second consecutive week of withdrawals as conflicts in Iran and oil price shocks worsened risk sentiment. In such environments, leverage is no longer just a market side issue but a major vulnerability.

Markets supported by stable spot demand tend to absorb psychological shocks gradually. Conversely, markets reliant on derivatives can adjust prices much faster when positions are liquidated and margin calls increase.

This is the biggest risk right now. Bitcoin can still continue to rise within a derivatives-driven structure, as has happened many times before.

But a market supported by leverage heavily depends on external conditions remaining stable. Just one macro shock, a massive ETF outflow, rising bond yields, a sharp stock market decline, or a shift in investor sentiment can quickly force leveraged positions to close faster than spot flows can re-enter.

This actually happened in February, when the crypto market experienced a wave of liquidations amid rising global risks. Although the external factors originated outside the crypto space, the speed of reaction was directly influenced by the market’s position structure.

High Liquidity, But Mostly “Synthetic Liquidity”

Bitcoin has spent years building a more robust institutional foundation. Spot Bitcoin ETFs have reached over $100 billion in assets under management, crypto derivatives on CME keep setting records, and more companies are adding BTC to their balance sheets.

However, better access to regulated crypto products doesn’t necessarily mean the daily trading infrastructure is more solid. Instead, it makes it easier for investors to quickly open large leveraged positions.

The market infrastructure has matured, but trading behavior remains fragile.

That’s why the gap between spot and derivatives trading must be closely monitored. It’s one of the best indicators of what’s truly supporting the market at any given time.

Currently, the main drivers are not retail spot demand or small investors, but leverage, hedging activities, and overall exposure via derivatives.

Bitcoin remains a high-liquidity market, but most of that liquidity is synthetic — and often the fastest to vanish under pressure.

Still, this doesn’t mean Bitcoin is destined to collapse. History shows Bitcoin can sustain resilience longer than many expect, and leverage can continue to fuel rallies as long as capital flows remain favorable.

However, the current structure is much more fragile than price movements suggest. If spot demand doesn’t return clearly and promptly, the market could continue upward but on a much weaker footing than most traders assume.