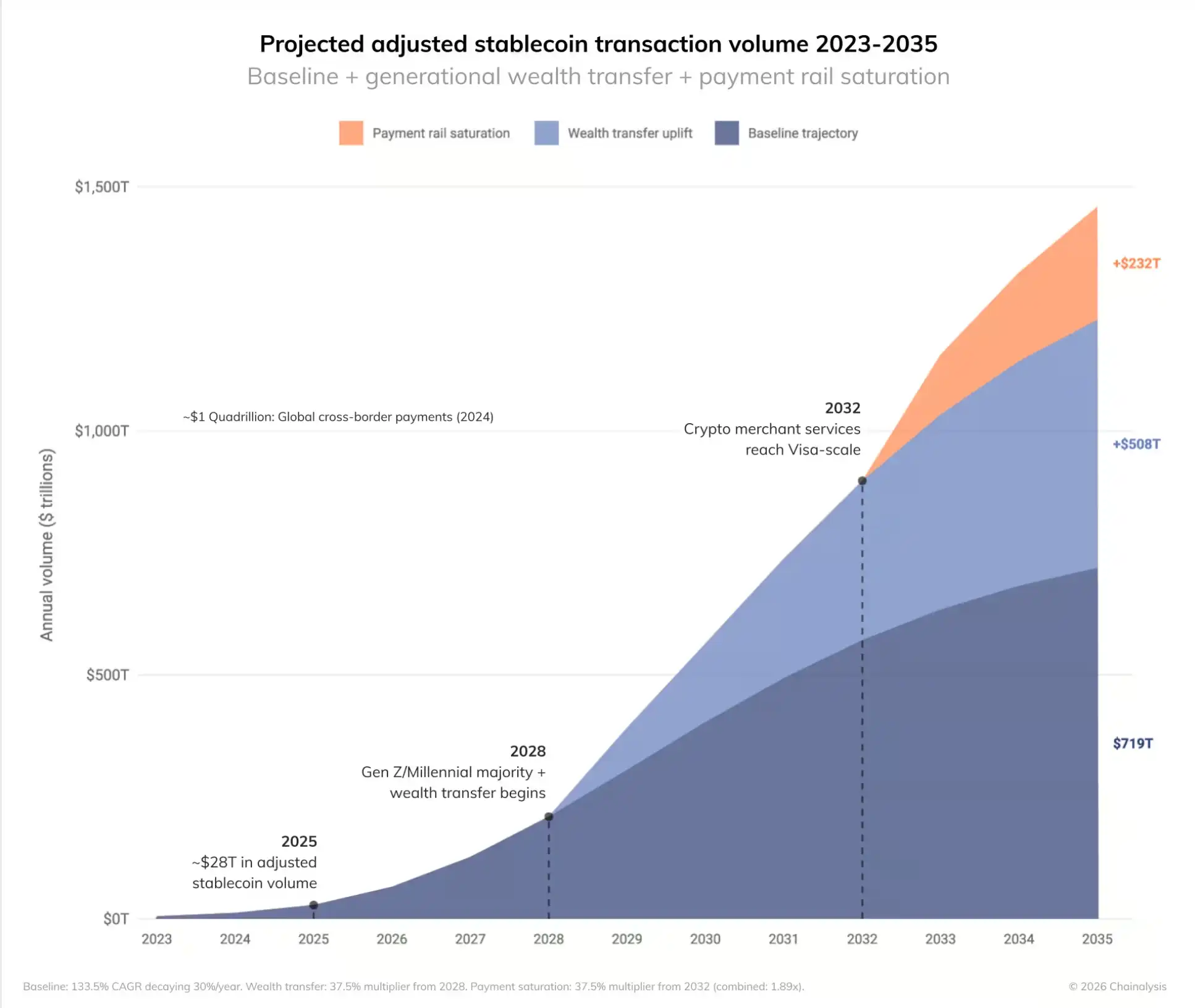

Blockchain analytics firm Chainalysis released a report on April 8 predicting that, by 2035, after adjusting for stablecoin-related factors, transaction volume under the baseline scenario will reach $719 trillion, with an upper bound of roughly $1,500 trillion. Chainalysis said that stablecoin payment volumes will at some point between 2031 and 2039 be comparable to Visa and Mastercard.

Two-Scenario Forecast: From $28 Trillion in 2025 to $719 Trillion in 2035

(Source: Chainalysis)

(Source: Chainalysis)

Chainalysis’ forecast is based on a strict filtering of “real economic activity”—after removing transaction noise, the real economic activity handled by stablecoins in the payments, remittances, and settlement domains in 2025 is about $28 trillion. Using this as the baseline, transaction volume can reach $719 trillion by 2035 with natural growth alone. If macro catalysts perform fully, the upper bound for transaction volume could reach $1.5 quadrillion, more than twice the baseline value.

This growth path implies that stablecoin’s real economic activity will grow by roughly 25 to 50 times within a decade. Driving this growth are two specific structural changes.

Two Major Growth Catalysts: Generational Wealth Transfer and Penetration of Payment Infrastructure

In its report, Chainalysis identified two core drivers propelling stablecoins from $28 trillion to $719 trillion and beyond:

Generational Wealth Transfer: Between 2028 and 2048, as much as $100 trillion in assets is expected to transfer from older generations to Millennials and Gen Z—two groups with significantly higher acceptance of digital assets than prior cohorts. This large-scale wealth transfer is expected to accelerate the adoption of crypto-native payment methods between 2031 and 2039.

Deep Penetration of Payment Infrastructure: As stablecoins become deeply integrated into merchants’ checkout processes and back-end payment systems, paying with stablecoins will become “invisible”—requiring no special actions, just like swiping a card naturally. AI-driven business models may also play a catalytic role in this process.

Chainalysis said its report indicates that structural shifts are already taking place, not merely remaining theoretical predictions.

Institutional Action Validates the Thesis: Strategic Bets by Stripe, Mastercard, and Standard Chartered

Large-scale adoption of stablecoins has gained endorsements from major financial institutions. Stripe’s acquisition of payments infrastructure company Bridge and Mastercard’s acquisition of BVNK clearly signal that stablecoins have grown from edge cases into a core component of payments infrastructure.

Standard Chartered said the growth rate of stablecoin usage is “beyond expectations,” and it assessed that stablecoins could drive demand for up to $1 trillion in U.S. Treasuries—directly linking payment growth to global capital flows.

On the regulatory front, research released by the White House this week found limited evidence that stablecoin yields cause real damage to bank lending, effectively countering outside concerns about deposit outflows. A crypto advisor in the Trump administration said stablecoins could channel deposits into the U.S. banking system rather than cause them to flow out, further strengthening the narrative framework of stablecoins as an integration with traditional finance rather than a disruptor.

Frequently Asked Questions

What is Chainalysis’ predicted number for stablecoins in 2035?

Chainalysis projects that by 2035, adjusted stablecoin transaction volume will reach $719 trillion under the baseline scenario; if macro catalysts play out fully, the upper bound could reach roughly $1.5 quadrillion ($1,500 trillion). The real economic activity of stablecoins in 2025 is about $28 trillion.

When might stablecoins reach transaction volume parity with Visa and Mastercard?

Chainalysis predicts that stablecoin payment volumes could be comparable to Visa and Mastercard at some point between 2031 and 2039. If adoption accelerates, this point could arrive earlier. Generational wealth transfer (expected to transfer $100 trillion between 2028 and 2048) is a key factor accelerating this process.

Which institutions have started betting on stablecoin payments infrastructure?

Stripe’s acquisition of Bridge and Mastercard’s acquisition of BVNK are landmark events signaling stablecoins’ entry into core payments infrastructure. Standard Chartered’s assessment holds that stablecoins could drive demand for up to $1 trillion in U.S. Treasuries, and the White House’s research also effectively refutes concerns that stablecoins lead to deposit outflows.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.