Amid the ongoing evolution of the DeFi “Curve Wars,” the function of CVX has expanded beyond that of a standard reward token. It now serves as a bridge connecting veCRV voting rights, protocol return allocation, gauge incentive competition, and governance decision-making, establishing itself as one of the most significant governance assets in the Curve ecosystem.

As Convex extends its reach to veToken ecosystems like Frax, FX Protocol, and Prisma, CVX’s governance scope and return structure have evolved from a single Curve yield optimization tool into a sophisticated DeFi incentive coordination layer.

CVX Token’s Protocol Role

CVX is primarily used for protocol governance, return incentives, and veCRV equity coordination. Rather than replacing Curve, Convex operates as a yield optimization layer within the Curve ecosystem, aggregating veCRV to enhance the capital efficiency of liquidity.

Traditionally, users seeking higher returns on Curve must lock CRV for extended periods to obtain veCRV and navigate complex governance and boost management. Convex simplifies this by aggregating veCRV, enabling users to earn higher returns without individually locking substantial CRV.

CVX’s core function is to connect “protocol governance” and “return incentives”. It represents both governance power within Convex and the protocol’s influence over veCRV incentive allocation during the Curve Wars. Accordingly, the value of CVX is closely tied to the amount of veCRV controlled by Convex, Curve’s return flows, and the protocol’s governance impact.

From an industry standpoint, CVX is typically viewed as a DeFi governance token, but its true nature is that of a composite asset—combining return rights, governance rights, and incentive coordination power.

CVX’s Role in Convex Finance

A central function of CVX is participation in Convex’s governance system. By locking CVX, users gain voting rights and can influence gauge weight allocation, protocol parameter changes, and aspects of return mechanism governance. Since Convex aggregates significant amounts of veCRV, CVX governance outcomes indirectly affect incentive flows across the Curve ecosystem.

Beyond governance, CVX is also integral to return distribution. Holders can stake CVX to earn a share of platform returns, including rewards from Curve, Frax, and related ecosystems. These rewards are typically converted to cvxCRV or other mapped assets before being distributed to CVX stakers.

CVX is also the primary reward asset within Convex’s incentive framework. When Curve LP users earn CRV returns via Convex, the protocol issues additional CVX proportional to CRV returns. This creates a “dual incentive model,” where users receive both Curve’s native returns and supplementary Convex rewards.

As Convex expands to other veToken ecosystems, such as FX Protocol and Prisma, CVX’s role is shifting from a Curve-only governance token to a cross-protocol incentive coordination tool.

CVX Issuance Mechanism and Supply Structure

CVX’s maximum supply is capped at 100 million, with issuance directly linked to CRV returns on the Convex platform. Unlike one-time token releases, CVX employs a dynamic release model—new CVX is minted proportionally as users earn CRV returns through Convex.

This “yield-driven minting” model means CVX growth is directly correlated with Convex platform activity, Curve yield volume, and LP participation. As Curve yield on Convex rises, CVX distribution accelerates.

However, the CVX minting ratio is not fixed indefinitely. The protocol’s “Cliff Reduction” mechanism gradually decreases the minting ratio as more CVX is released, slowing new issuance as supply nears its cap.

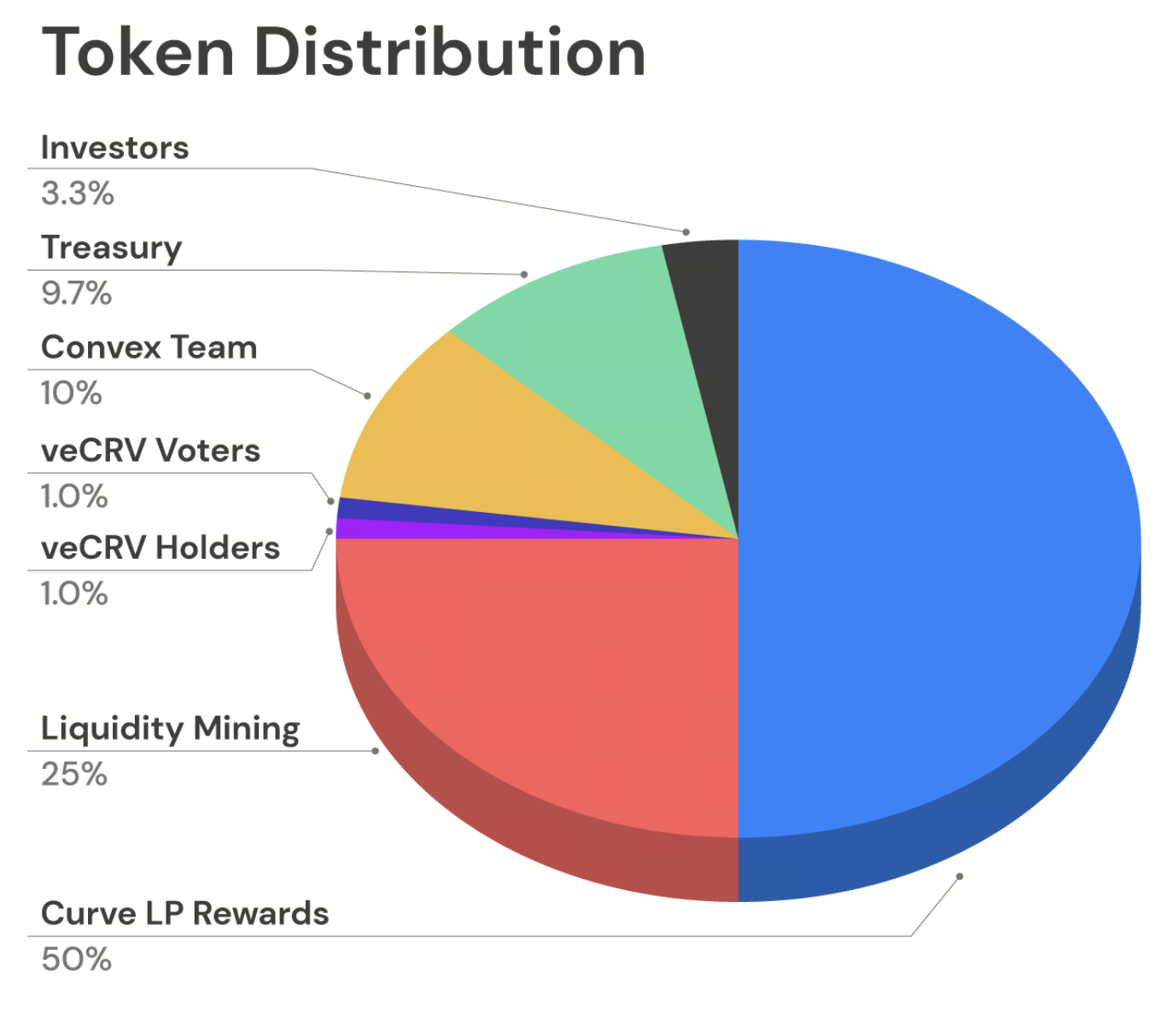

Initially, about half of all CVX was allocated to Curve LP incentives, with the remainder distributed among liquidity mining, the team, investors, the treasury, and veCRV community airdrops. This structure underscores Convex’s early reliance on Curve ecosystem expansion and veCRV aggregation.

Source: convexfinance.com

The Relationship Among CVX, veCRV, and cvxCRV

CVX, veCRV, and cvxCRV are deeply interconnected. veCRV is Curve’s governance-locked asset, while cvxCRV is a “tokenized veCRV” issued by Convex after locking CRV.

When users deposit CRV into Convex, the protocol permanently locks the CRV and converts it to veCRV. Users then receive cvxCRV at a 1:1 ratio, allowing them to benefit from veCRV yield potential without long-term self-locking.

CVX sits at the top of this structure. Through governance, CVX holders influence how Convex utilizes aggregated veCRV—including gauge voting direction and incentive allocation. Thus, CVX is essentially Convex’s “governance control layer” over veCRV.

This framework establishes a multi-tiered yield system built on veToken: Curve’s veCRV at the base, Convex’s cvxCRV in the middle, and CVX at the top, managing governance and incentive coordination.

Convex Finance Governance Mechanism

Convex governance centers on a Vote Locking mechanism. To participate, users must lock CVX for at least 16 weeks, earning corresponding voting rights. This model, similar to Curve’s veCRV structure, is a form of time-weighted governance.

Locked CVX not only enables governance participation but may also earn additional return distributions, as Convex redistributes a portion of platform returns to users who lock their tokens. Thus, Vote Locking serves as both a governance and yield incentive mechanism.

Governance focuses on veCRV utilization, gauge voting weights, and protocol upgrade proposals. Because Convex aggregates substantial veCRV, its governance outcomes directly impact liquidity incentive flows across Curve.

To prevent inactive locked positions from hindering governance efficiency, Convex introduced a “Kick” mechanism. If users fail to withdraw assets after unlocking, others can initiate a cleanup process and earn a small reward—ensuring active governance participation.

CVX Incentive Model and DeFi Yield Distribution Logic

The CVX incentive model is built atop Curve’s yield structure. Convex does not “create yield out of thin air”; instead, it aggregates veCRV to enhance Curve LP yield efficiency, redistributing a share of returns to CVX holders.

When users provide Curve LP liquidity through Convex, they receive CRV rewards. The protocol then distributes additional CVX based on the volume of CRV earned, tightly linking CVX distribution to Curve liquidity activity.

Additionally, CVX stakers receive a share of platform trading fee returns, sourced from Curve, Frax, FX Protocol, and other ecosystems, and distributed as cvxCRV, cvxFXS, and similar assets.

This forms a classic DeFi “yield cycle model”: Curve supplies base yield, Convex aggregates veCRV for enhanced returns, and CVX governs and redistributes incentives. As more veToken protocols integrate with Convex, this coordination framework is expanding across protocols.

CVX vs. CRV and Other DeFi Governance Tokens

CVX stands apart from traditional DeFi governance tokens in that its value is rooted not only in protocol governance but also in its robust veCRV aggregation capabilities. While CRV is Curve’s native governance token, CVX acts as a “second-layer governance asset” built atop the Curve incentive structure.

Unlike standard governance tokens focused solely on proposal voting, CVX emphasizes control over yield flows and incentive structures. Given Convex’s aggregation of veCRV, CVX governance decisions directly influence gauge incentive competition within Curve.

CVX’s yield model is also more complex than most governance tokens, which typically depend on a single protocol’s income. CVX draws incentives from multiple veToken ecosystems—including Curve, Frax, and FX Protocol—making its reward sources more diverse.

From an industry perspective, CRV is a foundational protocol governance token, while CVX represents a “governance aggregation layer asset” built on veCRV. This layered approach is a key factor in Convex’s rapid rise during the Curve Wars.

Summary

CVX is the core governance and incentive token of Convex Finance, fundamentally designed to coordinate veCRV aggregation, return distribution, and Curve’s incentive structure. Through vote locking, yield redistribution, and gauge governance, CVX has become one of the most influential governance assets in the Curve Wars.

Compared to traditional DeFi governance tokens, CVX places a stronger focus on “aggregated governance rights” and “yield coordination.” It not only integrates with Curve’s veCRV system but is also expanding to other veToken ecosystems like Frax and FX Protocol. As DeFi incentive models evolve, the “governance aggregation layer” exemplified by CVX stands as one of the most prominent cases within veToken economics.

FAQ

What is CVX?

CVX is the native governance token of Convex Finance, used for protocol governance, return distribution, and veCRV incentive coordination.

What is the difference between CVX and CRV?

CRV is the native governance token of Curve Finance, while CVX is a governance aggregation asset built on the Curve incentive system, primarily responsible for veCRV aggregation and yield coordination.

What is cvxCRV?

cvxCRV is the mapped asset users receive after depositing CRV into Convex, representing their equity in the Convex aggregated veCRV yield structure.

Why do I need to lock CVX?

Users must lock CVX to participate in Convex governance and earn a share of protocol return distribution.

What is the maximum supply of CVX?

CVX has a maximum supply of 100 million, with new issuance gradually slowing as the release schedule progresses.