As the DeFi market has grown rapidly, liquidity mining and on-chain market making have become important parts of the crypto market. Unlike traditional financial markets, which rely on professional market makers, the AMM model allows ordinary users to provide market liquidity by depositing assets into liquidity pools and earning a share of trading fees. Under this mechanism, however, liquidity providers also take on the risks created by on-chain asset price fluctuations.

As one of the most representative AMM protocols in DeFi, Uniswap has helped bring the liquidity pool model into widespread use. As a result, “impermanent loss” has become one of the risk concepts DeFi users pay the most attention to.

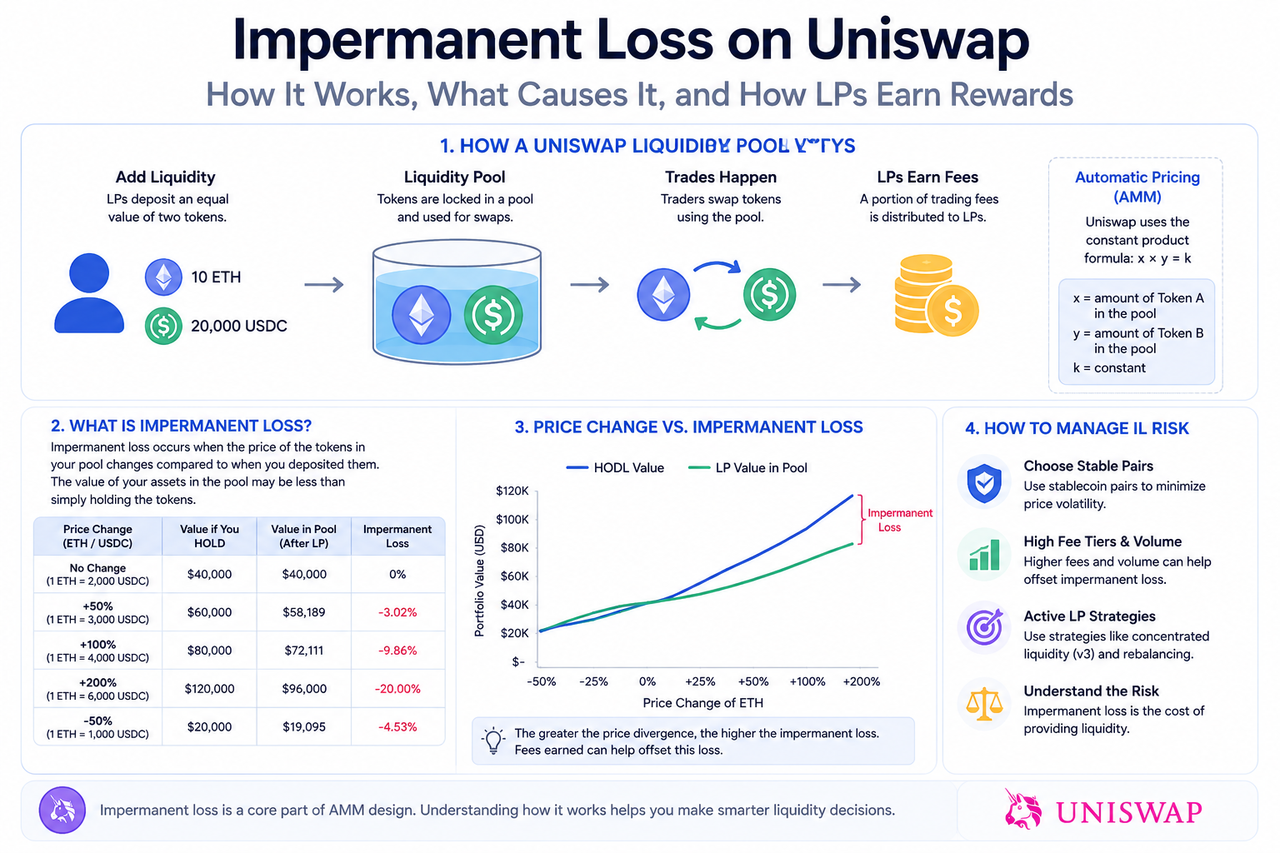

What Is Impermanent Loss?

Impermanent loss refers to a situation in which an LP provides assets to a liquidity pool and, because asset prices change, the final value of those assets becomes lower than it would have been if the LP had simply held them.

On Uniswap, liquidity pools automatically adjust the ratio of assets in the pool as asset prices change. When the price of an asset rises, that asset is gradually bought out of the pool; when its price falls, the pool accumulates more of it.

Therefore, when an LP withdraws liquidity, the quantity and composition of the assets they hold may have changed, creating a difference in value.

Why Does Impermanent Loss Happen?

The core reason impermanent loss occurs is the AMM mechanism.

Uniswap v2 uses the constant product formula:

$$x×y=$$

During trades, this formula continuously adjusts the ratio of assets in the pool to keep the product constant. When market prices change, arbitrage traders keep adjusting the pool price so that it moves closer to the price in the external market.

In this process, the asset composition actually held by the LP changes, so its value may become lower than the value of simply holding the assets.

How Do Uniswap LPs Earn Returns?

The main source of income for LPs is trading fees.

When users swap assets in a liquidity pool, the protocol charges a certain percentage as a fee and distributes it according to each LP’s share of the pool.

In markets with high trading volume, fee income may partly offset the risk of impermanent loss. As a result, an LP’s actual return usually depends on trading volume, market volatility, liquidity size, and changes in asset prices.

Pools with high trading volume are generally more likely to generate steady fee income, but pools containing more volatile assets may also produce more noticeable impermanent loss.

What Is the Difference Between Impermanent Loss in Uniswap v2 and v3?

Uniswap v3 introduced concentrated liquidity, which allows LPs to deploy funds within a specific price range.

This mechanism improves capital efficiency, but it also makes LPs more sensitive to price movements.

In v2, liquidity covers the entire price range, so risk is relatively spread out. In v3, however, if the price moves outside the range set by the LP, the funds may stop earning fees and become fully exposed to the risk of holding a single-sided asset.

Therefore, while v3 improves return efficiency, it also increases the complexity of actively managing liquidity.

What Factors Affect Impermanent Loss?

Impermanent loss is usually affected by the following factors:

-

Asset price volatility: the more sharply prices move, the more noticeable impermanent loss usually becomes.

-

Asset correlation: stablecoin pairs usually have lower impermanent loss because their price fluctuations are smaller.

-

Trading fee income: higher trading volume may increase LP returns, helping to partially offset losses.

-

Liquidity range settings: in v3, the price range directly affects the LP’s level of risk exposure.

How Can LPs Reduce the Risk of Impermanent Loss?

LPs usually reduce risk in several ways.

For example, some users prefer to choose:

In addition, some professional strategies combine dynamic position adjustment, automated rebalancing, and yield hedging mechanisms to reduce the impact of price volatility.

However, impermanent loss is part of the AMM mechanism itself, so it cannot be completely eliminated.

Does Impermanent Loss Always Become a Real Loss?

“Impermanent” means the loss has not been fully realized before asset prices return to their original level.

If the market price returns to the same ratio as when the LP deposited liquidity, impermanent loss may shrink or even disappear. But if the LP withdraws funds while prices are still deviating, the loss becomes an actual loss.

Therefore, whether impermanent loss is ultimately realized is closely tied to the path of price changes and the timing of the LP’s withdrawal.

Summary

Impermanent loss is one of the core risks in Uniswap and AMM liquidity mechanisms. At its core, it comes from the process by which liquidity pools automatically adjust asset ratios. Although LPs can earn income through trading fees, price volatility may still cause the value of their assets to fall below what they would have had by simply holding them.

As mechanisms such as Uniswap v3 improve capital efficiency, the return structure for LPs has also become more complex. Understanding how impermanent loss forms, what affects it, and how its risks are structured has become an essential foundation for participating in DeFi liquidity markets.

FAQs

Why does Uniswap create impermanent loss?

Because AMMs automatically adjust the ratio of assets in the pool, causing asset composition to change as market prices move.

Does impermanent loss always mean a real loss?

Not necessarily. If prices return to their original level, the loss may shrink. But if an LP withdraws funds early, it may become an actual loss.

Is impermanent loss higher in Uniswap v3?

Concentrated liquidity in v3 improves capital efficiency, but it also increases price range risk and the complexity of active management.

Can trading fees cover impermanent loss?

In some high-volume pools, fee income may partly offset losses, but it does not always cover them completely.

Do stablecoin pools have impermanent loss?

Yes. However, because price fluctuations are smaller, impermanent loss in stablecoin pools is usually relatively low.