Author: Trendverse Lab

Since the beginning of 2024, the stablecoin market has been undergoing a new change driven by structural innovation. After years of dominance by fiat-backed stablecoins like USDT and USDC, USDe, launched by Ethena Labs, has rapidly risen with its “no fiat support” synthetic stablecoin design, with a market capitalization that once surpassed 8 billion dollars, becoming the “high-yield dollar” in the DeFi world.

Recently, the Liquid Leverage staking activity launched by Ethena in collaboration with Aave has sparked heated discussions in the market: an annualized return approaching 50%. On the surface, it seems like a typical incentive strategy, but it may also reveal another signal worth paying attention to — the structural liquidity pressure faced by the USDe model during the ETH bull market.

This article will focus on the incentive activity, briefly explaining USDe/sUSDe and related platforms. It will analyze the systemic challenges hidden behind it from the perspectives of revenue structure, user behavior, and capital flow, and compare it with historical cases like GHO to explore whether future mechanisms have enough resilience to cope with extreme market scenarios.

1. Introduction to USDe and sUSDe: Synthetic Stablecoins Based on Crypto-Native Mechanisms

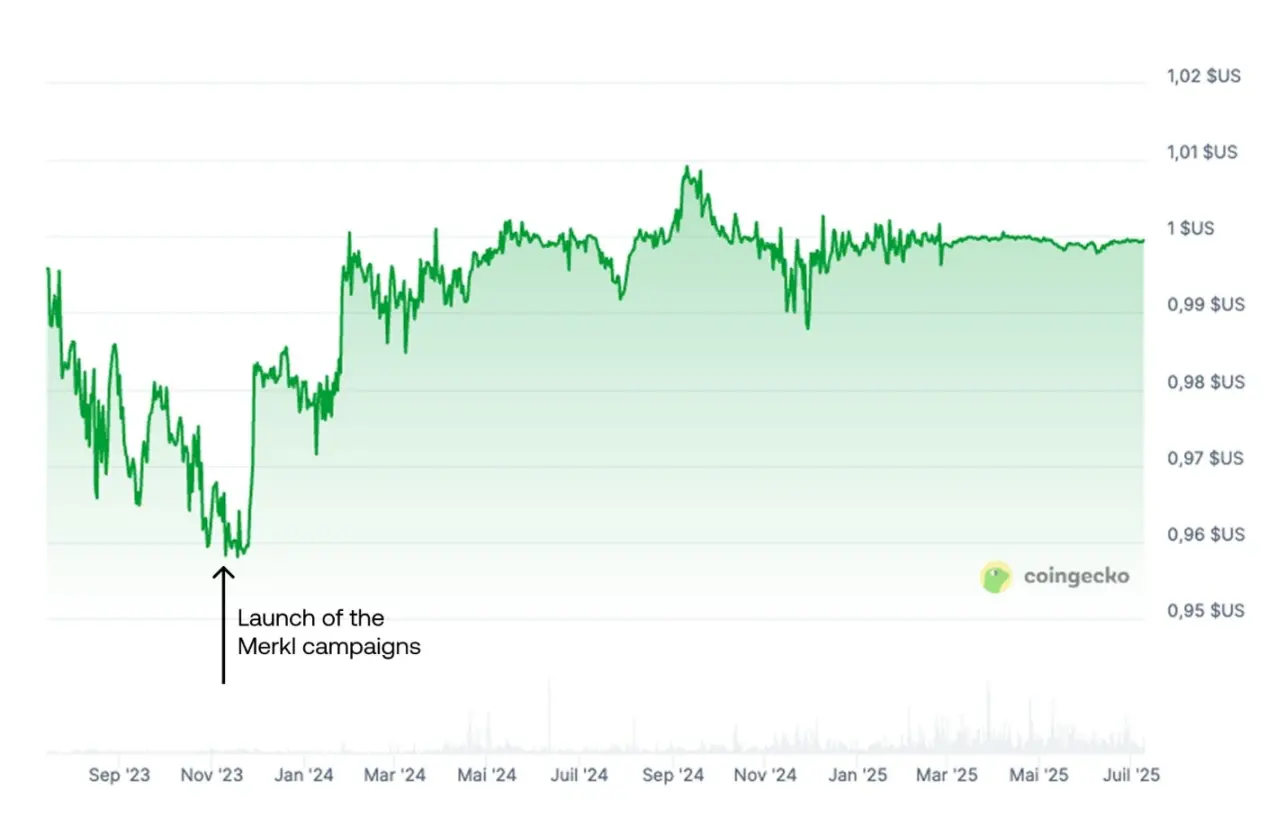

USDe is a synthetic stablecoin launched by Ethena Labs in 2024, designed to avoid reliance on traditional banking systems and issued currencies. As of now, its circulation scale has exceeded 8 billion USD. Unlike stablecoins supported by fiat reserves such as USDT or USDC, USDe’s anchoring mechanism relies on on-chain crypto assets, especially ETH and its derived staking assets (such as stETH, WBETH, etc.).

Image source: Coingecko

Its core mechanism is a “delta neutral” structure: on one hand, the protocol holds positions in assets such as ETH, while on the other hand, it opens equivalent perpetual short positions in centralized derivatives trading platforms. By utilizing a hedging combination of spot and derivatives, USDe achieves a net asset exposure close to zero, thereby stabilizing its price around 1 US dollar.

sUSDe is a representative token that users receive after staking USDe to the protocol, featuring automatic yield accumulation. Its yield sources mainly include returns from the funding rate in ETH perpetual contracts and derivative income generated from the underlying staked assets. This model aims to introduce a sustainable yield mechanism for stablecoins while maintaining their price peg.

2. Introduction to Aave and Merkl: The Collaborative System of Lending Protocols and Incentive Distribution Mechanisms

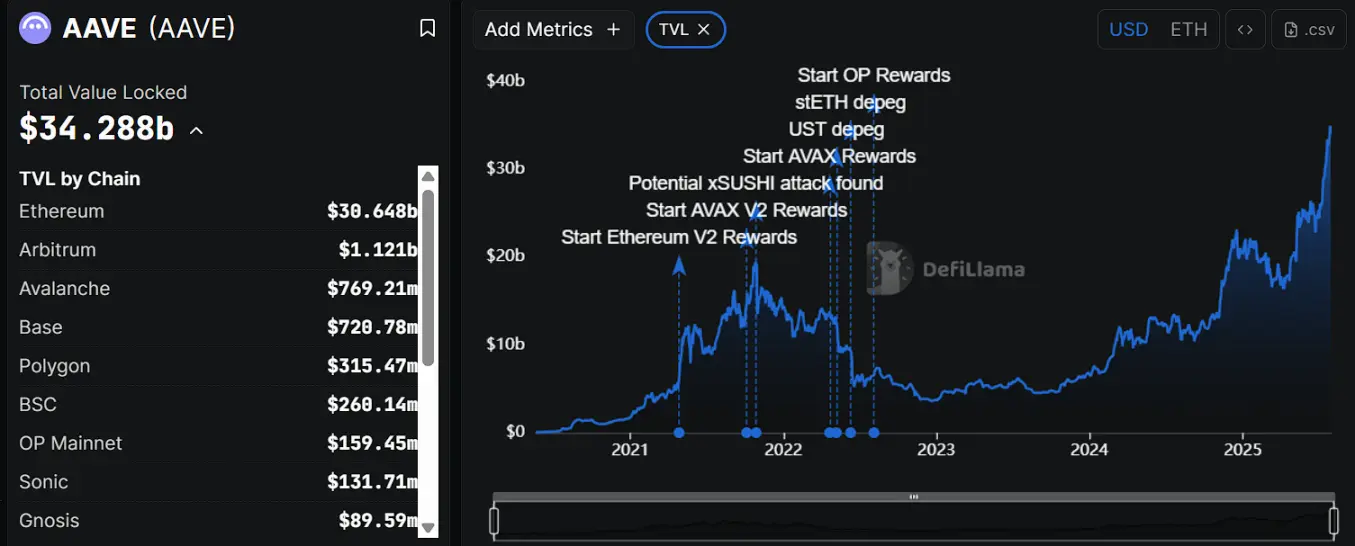

Aave is one of the oldest and most widely used decentralized lending protocols in the Ethereum ecosystem, dating back to 2017. It promoted the adoption of DeFi lending systems in the early days through the “flash loan” mechanism and a flexible interest rate model. Users can deposit crypto assets into the Aave protocol to earn interest or borrow other tokens by collateralizing their assets, all without intermediaries. Currently, the total locked value (TVL) of the Aave protocol is approximately $34 billion, with nearly 90% deployed on the Ethereum mainnet. The platform’s native token AAVE has a total market capitalization of about $4.2 billion, ranking 31st on CoinMarketCap.

Data source: DeFiLlama

Merkl is an on-chain incentive distribution platform launched by the Angle Protocol team, designed to provide programmable and conditional incentive tools for DeFi protocols. By using preset parameters such as asset type, holding duration, and liquidity contribution, protocol parties can accurately set reward strategies and efficiently complete the distribution process. To date, Merkl has served over 150 projects and on-chain protocols, with a total incentive distribution exceeding 200 million dollars, supporting multiple public chain networks including Ethereum, Arbitrum, and Optimism.

In this USDe incentive campaign jointly launched by Ethena and Aave, Aave is responsible for organizing the lending market, configuring parameters, and matching pledged assets, while Merkl is responsible for setting the reward logic and executing on-chain distribution.

In addition to the current USDe incentive collaboration, Aave and Merkl have previously established stable cooperative relationships in multiple projects, one of the most representative cases being the joint intervention on the GHO stablecoin’s de-pegging issue.

GHO is a native over-collateralized stablecoin launched by Aave, which can be minted by collateralizing assets such as ETH and AAVE. In the early stages of its launch, the token quickly fell below its peg due to limited market acceptance and insufficient liquidity, hovering in the $0.94 to $0.99 range for an extended period, losing its price peg to the US dollar.

To address this deviation, Aave, in collaboration with Merkl, has established a liquidity incentive mechanism for the GHO/USDC and GHO/USDT trading pairs on Uniswap V3. The incentive rules aim for “close to $1” and provide higher rewards to market makers who offer concentrated liquidity around $1, thereby guiding buy and sell depth to concentrate within the target range, creating a price stability wall on-chain. This mechanism has shown significant effectiveness in practice, successfully driving the GHO price gradually back up to near the $1 level.

This case reveals the essential role of Merkl in the stabilization mechanism: by using programmable incentive strategies to maintain the liquidity density of key trading ranges on the chain, similar to arranging “subsidized vendors” at market price anchor points. Only by continuously providing returns can a stable market structure be maintained. However, this also raises related issues: once the incentives are interrupted or the vendors withdraw, the support of the price mechanism may also fail.

3. Analysis of the Source Mechanism for 50% Annualized Returns

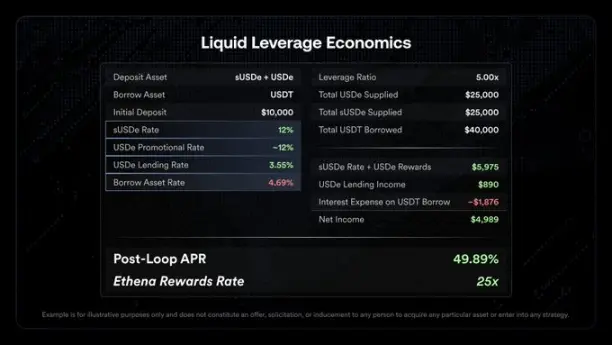

On July 29, 2025, Ethena Labs officially announced the launch of a feature module called “Liquid Leverage” on the Aave platform. This mechanism requires users to deposit sUSDe and USDe into the Aave protocol at a 1:1 ratio, creating a compound staking structure and thereby obtaining additional incentive rewards.

Specifically, qualified users can obtain three sources of income:

1 Merkl’s automatic distribution incentive USDe rewards (currently approximately 12% annualized);

The protocol yield represented by 2 sUSDe, which comes from the funding fees and staking returns of the delta-neutral strategy behind USDe;

3 Aave’s base deposit interest depends on the current market fund utilization rate and pool demand.

The specific participation process for this event is as follows:

1 Users can obtain USDe through the Ethena official website (ethena.fi) or decentralized exchanges (such as Uniswap);

2 Stake the USDe you hold on the Ethena platform to exchange for sUSDe;

3 Transfer an equal amount of USDe and sUSDe into Aave at a 1:1 ratio;

4 Enable the “Use as Collateral” option on the Aave page;

5 After the system detects compliance operations, the Merkl platform automatically identifies the address and regularly distributes rewards;

Image source: official Twitter

Official data, underlying calculation logic breakdown:

Assumption: $10,000 principal, 5x leverage, total borrowing of $40,000, using $25,000 as collateral for USDe and sUSDe respectively.

Leverage Structure Explanation:

The premise of this yield relies on a compound structure established by the “lending - depositing - continuing to lend” cycle, where the initial principal is used as collateral in the first round, and after the borrowed funds are lent out, the next round involves a two-way deposit of USDe and sUSDe. By leveraging the staking position 5 times, the total investment reaches $50,000, thereby amplifying rewards and base returns.

4. Does the incentive plan reveal that USDe and GHO face the same structural dilemmas?

Although both USDe and GHO are stablecoins issued based on the staking of crypto assets, there are significant differences in their mechanisms. USDe maintains its peg through a delta-neutral structure, with historical prices generally fluctuating steadily around $1, without experiencing a severe deviation like GHO’s drop to $0.94, nor has it faced a liquidity crisis similar to those that rely on liquidity incentives to restore prices. However, this does not mean that USDe is completely immune to risks; its hedging model itself has potential vulnerabilities, especially during severe market fluctuations or when external incentives are withdrawn, which could lead to stability shocks similar to those faced by GHO.

Specific risks are reflected in the following two aspects:

1 The funding rate is negative, and the protocol yield declines or even turns negative:

The main income of sUSDe comes from the LST earnings obtained from staking assets like ETH, along with the positive funding rate of the ETH short perpetual contracts established on centralized derivatives platforms. The current market sentiment is positive, with long positions paying interest to short positions, maintaining a positive yield. However, once the market turns weak and the number of short positions increases, the funding rate turns negative, requiring the protocol to pay additional fees to maintain hedged positions, which will reduce the yield and may even turn negative. Although Ethena has an insurance fund buffer, there remains uncertainty about whether it can cover negative yields in the long term.

2 Incentive Termination → Promotional Rate 12% Earnings Disappear Directly

The Liquid Leverage activities currently executed on the Aave platform offer additional USDe rewards for a limited time (approximately 12% annualized). Once the incentives end, the actual returns held by users will revert to the native sUSDe yield (funding fee + LST yield) and the deposit interest rate on the Aave platform, which may drop to a total range of 15-20%. In a high leverage structure (such as 5 times), after adding the USDT borrowing rate (currently at 4.69%), the profit margin is significantly compressed. In more severe cases, in an extreme environment where funding is negative and interest rates are rising, users’ net returns may be completely eroded or even turn negative.

If the incentives cease, ETH drops, and the funding rate turns negative simultaneously, the delta-neutral yield mechanism relied upon by the USDe model will face substantial impact, and the sUSDe yield may drop to zero or even turn negative. If this is accompanied by a large number of redemptions and selling pressure, the price anchoring mechanism of USDe will also face challenges. This “multiple negative overlap” constitutes the most critical systemic risk in the current Ethena architecture and may also be the deeper motivation behind its recent high-intensity incentive activities.

5. Will Ethereum’s price increase stabilize the structure?

Due to the stability mechanism of USDe relying on the spot staking of Ethereum assets and derivatives hedging, its fund pool structure faces systemic withdrawal pressure during rapid increases in ETH prices. Specifically, when the price of ETH approaches market expected highs, users tend to redeem their staked assets in advance to realize profits or shift to other assets with higher returns. This behavior gives rise to a typical “ETH Bull Market → LST Outflow → USDe Contraction” chain reaction.

From DeFiLlama data, it can be observed that the TVL of USDe and sUSDe declined simultaneously during the ETH price surge in June 2025, and there was no increase in annualized yield (APY) accompanying the price rise. This phenomenon contrasts with the previous bull market (late 2024): at that time, after ETH reached its peak, the TVL gradually retreated, but the process was relatively slow, and users did not collectively redeem their staked assets early.

In the current cycle, both TVL and APY are declining simultaneously, reflecting an increasing concern among market participants about the sustainability of sUSDe yields. When price volatility and changes in funding costs introduce potential negative yield risks to delta-neutral models, user behavior demonstrates higher sensitivity and responsiveness, with early exits becoming the mainstream choice. This phenomenon of capital withdrawal not only weakens the expansion capacity of USDe but also further amplifies its passive tightening characteristics during the ETH bullish cycle.

Summary:

In summary, the current annualized yield of up to 50% is not the norm for the protocol, but rather the result of multiple external incentives (Merkl airdrop + Aave collaboration) in a phased manner. Once risks such as high ETH price fluctuations, termination of incentives, and negative funding rates are concentrated and released, the delta-neutral yield structure relied upon by the USDe model will face pressure, and sUSDe yields may quickly converge to 0 or turn negative, thereby impacting the stability anchoring mechanism.

Recent data shows that the TVL of USDe and sUSDe has declined simultaneously during the ETH uptrend, and the APY has not increased in tandem. This “draining during the rise” phenomenon indicates that market confidence is beginning to price in risks in advance. Similar to the “pegging crisis” that GHO once faced, the current liquidity of USDe is largely dependent on ongoing subsidy stabilization strategies.

When will this incentive game come to an end, and whether it can secure enough structural resilience adjustment windows for the protocol, may become the key test of whether USDe truly has the potential to be the “third pole of stablecoins.”