Author: Frank, MSX Research Institute

In the past, trading US stocks meant not being able to sleep at night; does that mean I won't be able to sleep during the day in the future?

When the cryptocurrency market has become accustomed to the 7×24 never-sleep rhythm, Nasdaq, standing at the core hub of TradFi, can no longer sit still.

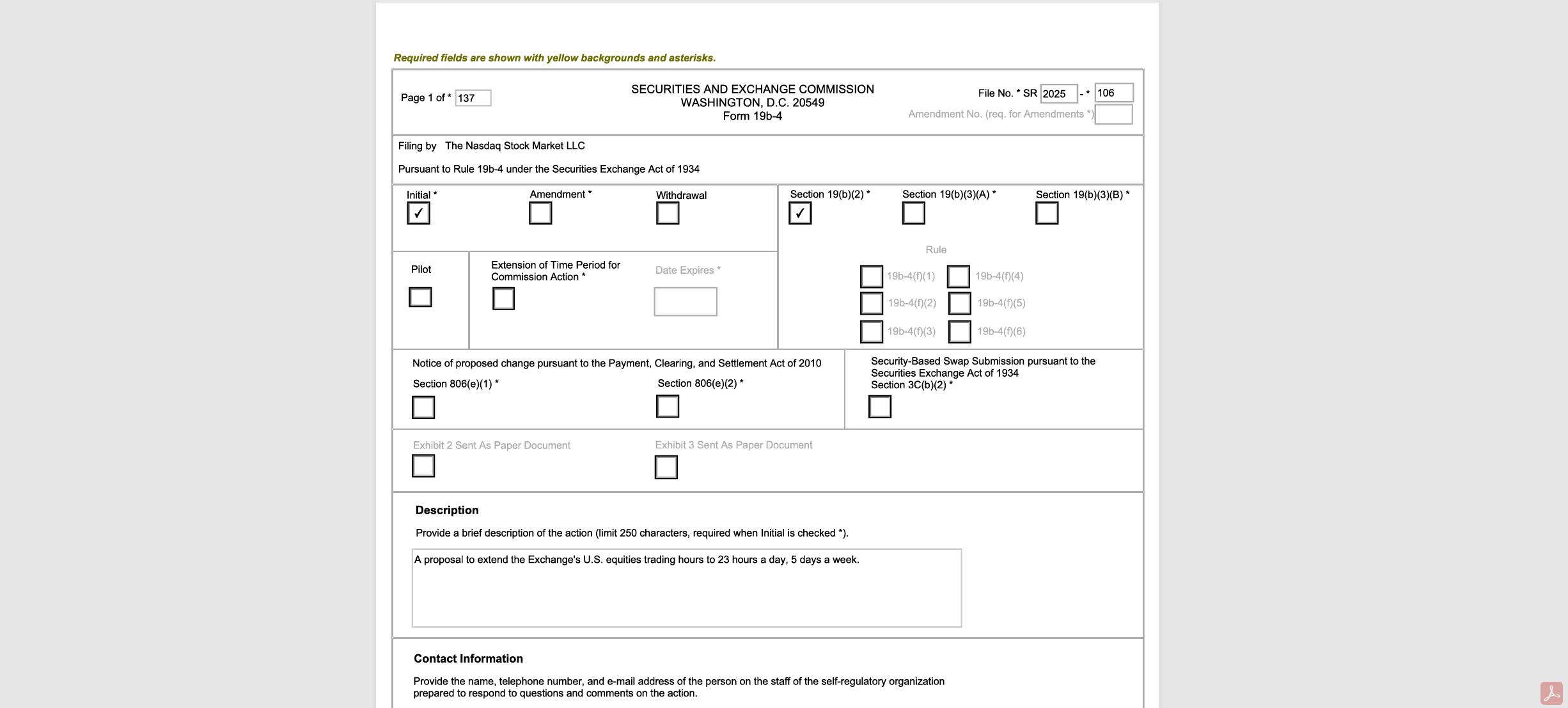

On December 15, Nasdaq officially submitted documents to the U.S. Securities and Exchange Commission (SEC), planning to extend trading hours from the current 5 days a week, 16 hours a day (pre-market/market/after-hours) to 5 days a week, 23 hours a day (daytime/nighttime).

Once approved, U.S. stocks will trade from Sunday night at 21:00 until Friday night at 20:00, with only a 1-hour (20:00-21:00) market closure window each day. The official reason is quite respectable, stating “to meet the growing demand from Asian and European investors, allowing them to trade during non-traditional hours.”

But if we peel back the layers, we will find that the logic behind this goes far beyond that. Nasdaq is clearly conducting extreme stress tests for the future tokenization of stocks, and we are gradually piecing together a continuously advancing timeline:

Nasdaq and the US financial markets are preparing for a “non-closing financial system.”

1. From 5×16 to 5×23: The “Last Hour” Approaching the Limits of TradFi

On the surface, this is merely an extension of trading time, but from the perspective of various participants in TradFi, this step has nearly pushed the technical carrying capacity and collaborative ability of the existing financial infrastructure system to its physical limits.

As we all know, stock trading under the TradFi system is a precisely meshed gear assembly, aside from Nasdaq, stakeholders also include brokerages, clearing institutions, regulatory bodies, and even the listed companies themselves. This means that to support a 23-hour trading system, all market participants need to communicate thoroughly and carry out deep transformations around all aspects such as clearing and settlement and collaborative systems:

- Brokers and dealers must extend their customer service, risk control, and trading maintenance systems to operate around the clock, resulting in a direct increase in operational and labor costs;

- The clearing organization (DTCC) needs to simultaneously upgrade the trading coverage time and clearing and settlement system, extending service hours to 4 AM to comply with the new rule of “next-day settlement for night trading” (trading from 21:00 to 24:00 will be counted towards the next day);

- Public companies must also recalibrate the disclosure rhythm of financial reports or significant announcements, and investor relations and market participants need to gradually adapt to the new reality of “significant information being priced in real-time by the market during non-traditional periods”;

Of course, for us in the East 8 Zone, trading in US stocks used to mainly take place in the late night or early morning. The future model of 5 days × 23 hours means that we can participate in real-time without staying up late, which is a significant advantage. However, it also raises a soul-searching question — since the decision to reform has been made, why can't we achieve 7×24 all at once, instead of leaving this awkward 1 hour?

According to Nasdaq's public disclosures, the 1-hour downtime is primarily used for system maintenance, testing, and trade settlement. This highlights the “Achilles' heel” of the traditional financial architecture, namely that under the existing centralized clearing and settlement system (based on DTCC and broker/bank systems), a physical downtime is necessary for data batching and margin settlement and guarantees.

Just like a bank branch has to close its books after work every day, from another perspective, this 1 hour can also be considered a “fault tolerance window” in the real world. Although it requires a significant investment in personnel shift costs and system maintenance costs, it also provides a necessary buffer for the upgrade of various systems under the current financial infrastructure, synchronization of clearing and settlement, fault isolation, and risk management.

However, compared to the past, the remaining 1 hour for the future imposes almost harsh requirements on the collaborative ability across roles in the entire TradFi industry, akin to an extreme pressure test.

In contrast, blockchain-based cryptocurrencies and tokenized assets rely on decentralized ledgers and smart contract atomic settlements, inherently possessing a 7×24×365 all-weather trading gene, with no closing hours, no need for market halts, and no need to squeeze critical processes into a fixed end-of-day window.

This also explains why Nasdaq is struggling to challenge the limits, not because it suddenly realized the importance of being “considerate” towards Asian users, but rather due to the situation— as the boundaries between the 7×24 cryptocurrency market and traditional financial markets become increasingly blurred, the incremental trading demand for traditional exchanges increasingly comes from global funds across different time zones and a longer duration of liquidity coverage.

It can be said that by 2025, tokenization is already on the verge of happening, with players like Nasdaq having already laid out their strategies behind the scenes. Therefore, from this perspective, the 23-hour trading system is not an isolated rule change of 'opening a few more hours,' but more like a transitional state that paves the way for stock tokenization, on-chain settlement, and a 7×24 global asset network:

Without overturning the existing securities laws and the National Market System (NMS), we should first align the trading system, infrastructure, and participant behavior towards a rhythm that is “closer to on-chain”—to prepare and pave the way for more radical goals in the future (such as more continuous trading, shorter settlement cycles, and even on-chain clearing and tokenized delivery).

Imagine, once the SEC approval is granted and the 23-hour trading system begins to operate and gradually becomes the norm, the market's patience threshold and reliance on “trade anytime, instant pricing” will be raised. How far can we be from that true 7×24 conclusion?

When the tokenization of US stocks officially lands, the global financial system will smoothly transition to that truly “never-closing” future.

2. What profound impacts will this have on the market?

Objectively speaking, the “5×23” model could be a structural shock affecting the global TradFi ecosystem.

In terms of time breadth, it significantly expands the time boundaries of trading, which is undoubtedly a substantial benefit for investors across different time zones, especially in the Asian market; however, from the perspective of market microstructure, it also introduces new uncertainties in terms of liquidity distribution, risk transmission, and pricing power, easily triggering concerns about the “sustainability” of global liquidity.

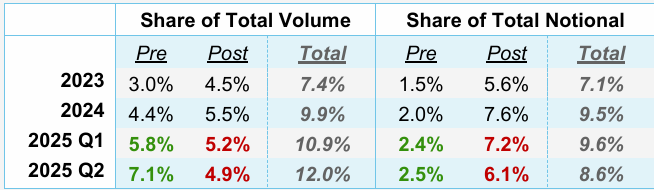

In fact, in recent years, the activity in the non-traditional trading hours of the US stock market (pre-market and after-hours) has indeed shown explosive growth.

Data from the New York Stock Exchange shows that in the second quarter of 2025, the trading volume during non-trading hours exceeded 2 billion shares, with a transaction value of 62 billion USD, accounting for 11.5% of U.S. stock trading for that quarter, setting a historical record. At the same time, transaction values on nighttime trading platforms such as Blue Ocean and OTC Moon continue to rise, and after-hours trading is no longer a fringe phenomenon, but has become a new battleground that mainstream capital cannot ignore.

Source: New York Stock Exchange

This is essentially a concentrated release of the real demand from global traders, especially retail investors in Asia, to “trade US stocks in their own time zone.” From this perspective, what Nasdaq is attempting to do is not to create demand, but to re-utilize the night trading that was originally scattered in the over-the-counter, low transparency environment, and “recapture” the rights to centralize and regulate it within a compliant exchange system, reclaiming the compilation rights that had been lost in the dark.

But the problem is that the “5×23” trading does not necessarily lead to higher quality price discovery; it is more likely to present a highly commendable double-edged sword situation:

- First, there is the risk of “fragmentation” and “dilution” of liquidity: Although extending trading hours theoretically attracts more cross-timezone capital, in reality, it also means that limited trading demand is fragmented and diluted over a longer timeline. This is particularly true during the “night” session under the “5×2 3” model, where the corresponding trading volume in U.S. stocks is already lower than during regular hours. The extension may further lead to wider spreads, insufficient liquidity, increased trading costs and volatility, and even make it easier to manipulate the market during periods of thin liquidity.

- Secondly, there is the potential change in pricing power structure: As mentioned earlier, Nasdaq hopes to absorb scattered orders that have been diverted to off-exchange platforms such as Blue Ocean and OTC Moon through the “5×23” model. However, for institutions, liquidity fragmentation has not disappeared; it has simply shifted from “off-exchange dispersion” to “on-exchange time-sharing,” which poses higher costs for risk control and execution models.

- Finally, the possibility of black swan risk being amplified due to “0 latency”: In a 23-hour trading framework, significant unexpected events (whether it's a sudden drop in performance, regulatory statements, or geopolitical conflicts) can be immediately converted into trading orders. The market no longer has the buffer period of “sleeping through the night to digest”. In the relatively thin liquidity environment of night trading, this immediate reaction can more easily trigger a chain of black swan events characterized by gap openings and severe fluctuations in an exponential manner;

Therefore, the author pointed out in the above text that trading under the “5×23” model is by no means as simple as “just trading for a few more hours”. It is not merely a question of “smaller or larger risks”, but rather a systematic stress test on the price discovery mechanism, liquidity structure, and distribution of pricing power of TradFi.

Everything is paving the way for that “never closing” tokenized future.

Three, the whole chess game of Nasdaq: all the groundwork points to On-Chain

If we extend our perspective and connect the recent intensive actions of NASDAQ, we will be more convinced that this is a strategic puzzle with subtle layers, where the core objective aims to enable stocks to ultimately possess the ability to circulate, settle, and price like Tokens.

To this end, NASDAQ has chosen a path of gentle reform with a strong traditional financial style, and the evolution logic of the roadmap is extremely clear, advancing step by step.

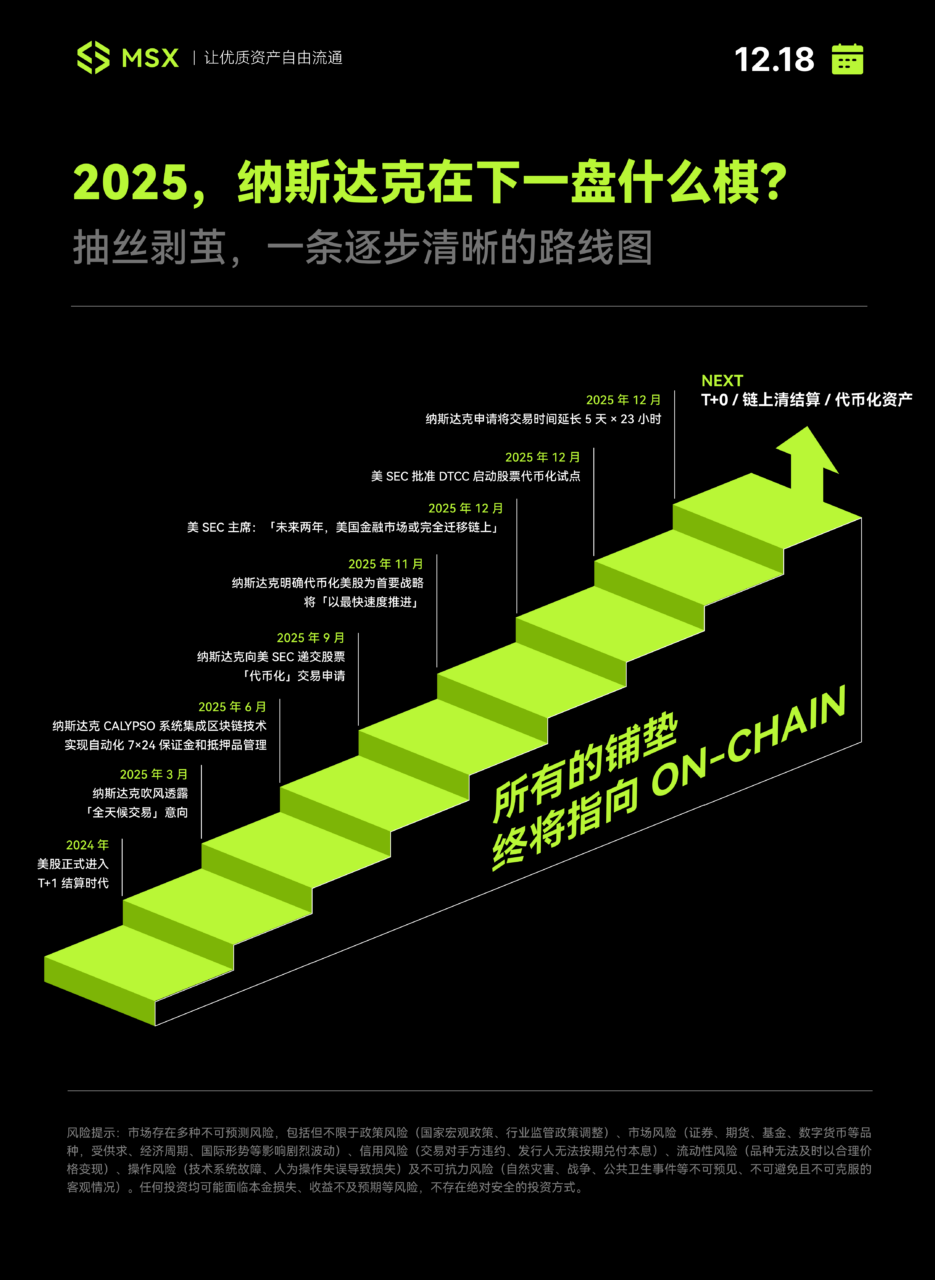

The first step occurs in May 2024, when the U.S. stock settlement system officially shortens from T+2 to T+1, which is a seemingly conservative yet crucial infrastructure upgrade; shortly thereafter, in early 2025, Nasdaq begins to release signals of its intention for “around-the-clock trading,” hinting at plans to launch uninterrupted trading services five days a week in the second half of 2026.

Subsequently, Nasdaq shifted its reform focus to a more obscure yet crucial backend system—the Calypso system, which integrates blockchain technology for 24/7 automated margin and collateral management. This step has almost no apparent change for ordinary investors, but it is a very clear signal for institutions.

By the second half of 2025, Nasdaq will begin to make positive progress in terms of systems and regulatory aspects.

Formally submitted a stock “tokenization” trading application to the U.S. SEC in early September, and in November, tokenizing U.S. stocks became the primary strategy, which will be “advanced at the fastest speed.”

Almost simultaneously, SEC Chairman Paul Atkins stated in an interview with Fox Business that tokenization is the future direction of capital markets. By putting securities assets on the blockchain, clearer ownership verification can be achieved. He anticipates that “within about 2 years, all markets in the United States will migrate to operate on-chain, achieving on-chain settlement.”

Against this backdrop, Nasdaq submitted an application for a 5×23 hour trading system to the SEC in December 2025.

From this perspective, the “23-hour trading system” extended trading hours by NASDAQ is not a single-point reform, but a necessary step in its stock tokenization roadmap. This is because future tokenized assets will inevitably seek 7×24 hour round-the-clock liquidity, and the current 23 hours is the “transitional state” closest to the on-chain rhythm.

What is most intriguing is that the regulators (U.S. SEC), infrastructure (DTCC), and trading venues (Nasdaq) demonstrated a highly coordinated rhythm in 2025:

- The SEC's Easing and Positioning: On one hand, it continues to loosen regulations, while on the other, it consistently releases expectations of “full on-chain” through high-level interviews, injecting certainty into the market;

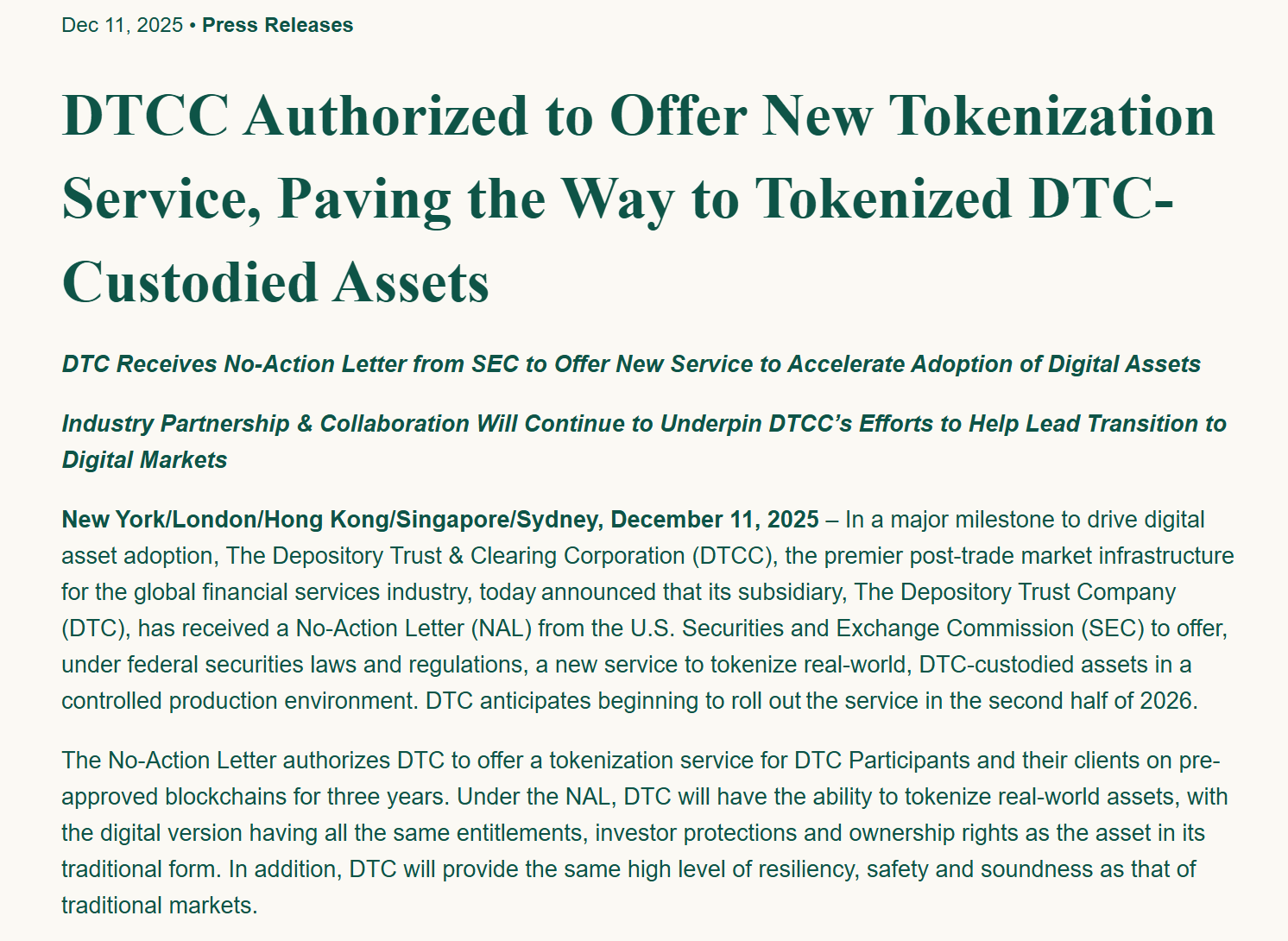

- DTCC Foundation: On December 12, DTCC's subsidiary, the Depository Trust Company (DTC), received a no-action letter from the SEC, approving its provision of tokenization services for real-world assets in a controlled production environment, with plans for a formal launch in the second half of 2026 to address the core issues of clearing and custody compliance;

- NASDAQ Surge: Official announcement of tokenized stock plan, priority level maxed out, submitted a 23-hour trading application, attracting global liquidity;

Source: DTCC Official Website

When these three lines are placed on the same timeline, the tacit understanding of this collaboration is hard not to lead one to a conclusion:

This is not a coincidence or a sudden whim from Nasdaq, but a highly coordinated and continuously advancing institutional project. Nasdaq and the American financial market are making a final push for a “non-closing financial system.”

Written at the end

Of course, once Pandora's box is opened, “5×23 hours” is just the first step.

After all, once the demands of human nature are released, they become irreversible. Therefore, since U.S. stocks can be traded at midnight, users will inevitably ask: Why do I still have to endure that 1-hour interruption? Why can't I trade on weekends? Why can't I settle in USDT instantly?

As the appetite of global investors is thoroughly aroused by “5×23 hours”, the existing flawed structure of TradFi will face its final cut, and only the 7×24 native tokenized assets can fill that last hour's gap. This is also why, in addition to Nasdaq, players like Coinbase, Ondo, Robinhood, and MSX are all racing — and being engulfed by the tide.

The future is still far off, but there is not much time left for the “old clock.”

(The above content is excerpted and reproduced with the authorization of our partner PANews, original link | Source: MSX Research Institute __)

_

Disclaimer: This article is for providing market information only. All content and opinions are for reference only and do not constitute investment advice, nor do they represent the views and positions of the blockchain. Investors should make their own decisions and trades, and the author and the blockchain will not bear any responsibility for any direct or indirect losses incurred by investors' trades.

_

Tags: 5 x 23 Nasdaq tokenized all-weather cryptocurrency blockchain investment Nasdaq US stocks Nasdaq