China’s gradual withdrawal from U.S. government bonds is shifting from a quiet trend within the economy to a clearer risk management signal. The Bitcoin market is closely monitoring for the next “domino effect.”

The direct catalyst for the new wave of concern appeared on February 9, when Bloomberg reported that Chinese regulators are advising commercial banks to limit their exposure to U.S. Treasury bonds due to concentrated risk and increased volatility.

This guidance immediately drew market attention to the massive scale of U.S. bonds held by Chinese institutions. According to the State Administration of Foreign Exchange (SAFE), as of September, Chinese banks held approximately $298 billion in USD-denominated bonds.

However, the biggest blind spot—and also the source of unease—is that no one knows exactly how much of these are U.S. Treasury bonds and how much are other USD debt instruments.

This regulatory pressure is not happening in isolation. It continues the strategy of withdrawing from U.S. bonds that has been ongoing for over a year, as clearly reflected in Beijing’s official accounts.

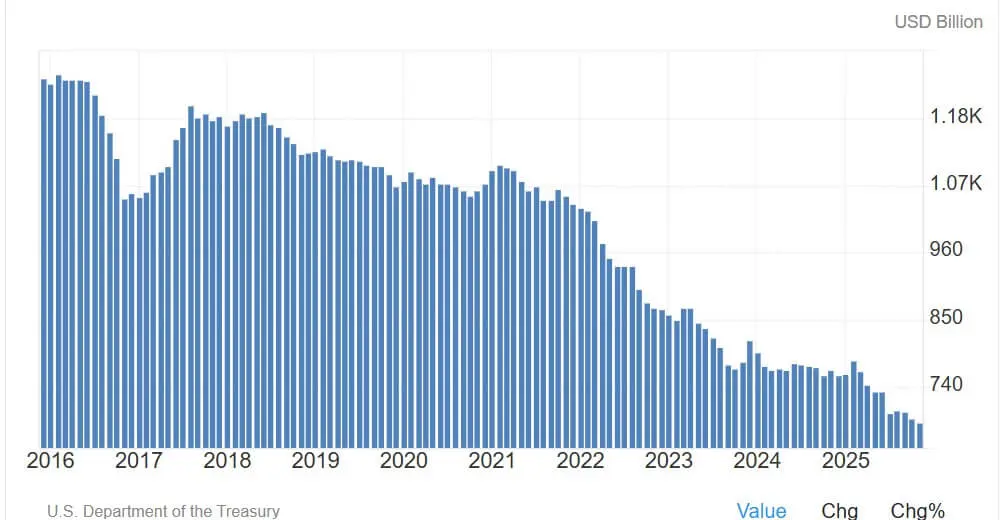

U.S. Treasury Foreign Holdings data from the U.S. Treasury Department shows that China’s holdings of U.S. Treasury bonds fell to $682.6 billion in November 2025—marking the lowest in over a decade.

This trend has accelerated over the past five years, as China actively reduces its dependence on the U.S. financial market.

The overall picture is quite clear: Eastern buying power is weakening, both in trade channels and through state holdings.

U.S. Treasury bonds held by China (Source: Trading Economics)## Why Should Bitcoin Care About U.S. Bond Yields?

U.S. Treasury bonds held by China (Source: Trading Economics)## Why Should Bitcoin Care About U.S. Bond Yields?

The risk to Bitcoin does not lie in China “crashing” the U.S. bond market. The market size is too large: with $28.86 trillion in tradable debt, China’s $682.6 billion holdings account for only about 2.4%.

The real danger is more subtle. If declining foreign capital flows force yields higher through the “term premium” channel, this will directly tighten financial conditions—an environment that highly volatile assets like crypto depend on heavily.

On the day of the news surge, the 10-year U.S. Treasury yield hovered around 4.23%. This level itself isn’t a crisis, but the concern lies in its upward trajectory.

A re-pricing process can still be controlled. Conversely, an uncontrolled spike caused by a “buyer strike” could trigger a wave of deleveraging across interest rates, equities, and crypto markets.

The Kansas City Fed’s 2025 economic report estimates that just a one-standard-deviation liquidation by foreign investors could push U.S. Treasury yields up by 25–100 basis points.

Notably, yields could rise even without a major sell-off, simply if demand for new issuance weakens.

In a more extreme scenario, a 2022 NBER study shows that a $100 billion sell-off by foreign entities could immediately increase 10-year yields by over 100 basis points before easing.

This is not a baseline forecast but a reminder that in liquidity shocks, market positions often overshadow fundamentals.

Real Yields and Financial Conditions: Key Points for Bitcoin

Since 2020, Bitcoin has largely traded as a “macro duration asset.” In this context, higher yields and tighter liquidity typically exert downward pressure on risky assets, even if the shock originates from the interest rate markets.

Therefore, real yields are a crucial variable. On February 5, the 10-year U.S. TIPS yield was around 1.89%, indicating increasing opportunity costs for holding non-yielding assets like Bitcoin.

However, the bearish camp faces a “trap”: overall financial conditions have not signaled a crisis. The Fed Chicago’s National Financial Conditions Index was at -0.56 for the week ending January 30, indicating a still-loose environment.

The nuance is that markets can tighten significantly from a “comfortable” state without triggering systemic crises.

For crypto, this intermediate tightening phase is often enough to push Bitcoin lower without requiring Fed rescue measures.

Recent price movements reflect this sensitivity. Last week, Bitcoin dipped below $60,000 in a risk-off wave, then rebounded above $70,000 as sentiment stabilized. As of February 9, Bitcoin continued to recover, acting as a high-beta indicator of global liquidity.

Four Scenarios Traders Are Watching in China–Yield–Bitcoin Dynamics

Market focus isn’t just on whether China is selling, but on how quickly and how the market absorbs that supply. The impact on Bitcoin depends entirely on the level of USD liquidity stress.

Scenario 1: Controlled Risk Reduction (Base Case)

Chinese banks gradually reduce purchases, mainly due to maturity and reallocation, not panic selling.

U.S. yields rise slowly by 10–30 basis points, primarily driven by the term premium. Bitcoin faces mild resistance, with main drivers still being U.S. economic data and Fed policy expectations.

Scenario 2: Strong Repricing of Term Premium (Macro Negative)

If markets interpret China’s moves as a structural change in foreign demand, yields could increase by 25–100 basis points.

If real yields lead the move, financial conditions could tighten enough to reduce risk appetite, weakening crypto due to higher capital costs, reduced liquidity, and risk-parity deleveraging.

Scenario 3: Liquidity Shock with Disorderly Deleveraging (Tail Risk)

A rapid wave of position unwinding, whether politically motivated or mass action, even if not led by China, could cause nonlinear volatility.

The “stress episode” framework, exemplified by a $100 billion sell-off pushing yields over 100 basis points, is used by traders to gauge extreme risk.

In this scenario, Bitcoin could initially plunge due to forced selling, then recover if policymakers deploy liquidity support.

Scenario 4: Stablecoin Turnaround (Unrecognized Risk)

Paradoxically, as China withdraws, crypto might advance.

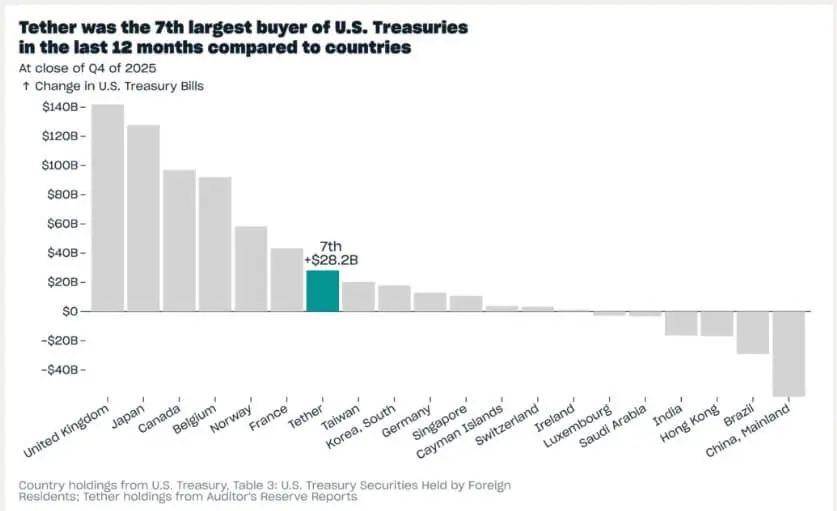

According to DeFiLlama, stablecoin market cap is about $307 billion. Tether alone reports holding $141 billion in U.S. Treasuries and related instruments—almost one-fifth of China’s holdings.

Tether even claims to be among the top 10 largest buyers of U.S. bonds last year.

If stablecoin supply remains stable, crypto capital could indirectly “self-sustain” by supporting demand for short-term debt, though Bitcoin would still face pressure if overall financial conditions tighten.

Tether’s U.S. Treasury bond purchases (Source: Tether)## Policy “Backstop” Factor: Rising Yields as a Positive Signal for Bitcoin

Tether’s U.S. Treasury bond purchases (Source: Tether)## Policy “Backstop” Factor: Rising Yields as a Positive Signal for Bitcoin

The final pivot point in the “rising yields–Bitcoin falling” correlation lies in market functions.

If yields increase to levels threatening the operation of the Treasury market, the U.S. has tools to intervene. An IMF study shows that bond buyback programs can quickly restore order in stressed segments.

This reflexivity is what crypto traders rely on: in a major bond market shock, Bitcoin’s sharp initial decline often paves the way for a recovery once liquidity is restored through supportive measures.

Currently, China’s $682.6 billion holdings are not necessarily a “sell signal” but a measure of systemic fragility.

It reminds us that demand for Treasury bonds is becoming sensitive at the margin, and Bitcoin remains the clearest real-time indicator to distinguish between a healthy re-pricing process and the onset of a more dangerous tightening regime.

Vương Tiễn