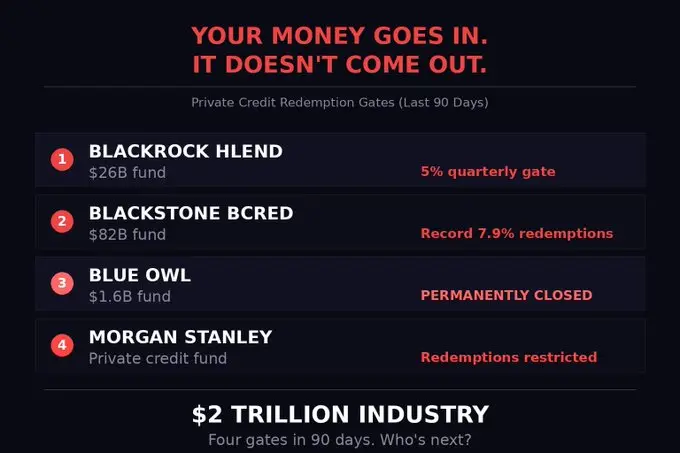

Since late February, five major private credit fund managers, including Morgan Stanley, have consecutively restricted or suspended investor redemptions within three weeks. Analysts believe that trapped investors may be forced to turn to highly liquid assets like Bitcoin and Ethereum to raise funds; meanwhile, the Federal Open Market Committee (FOMC) will hold a rate decision meeting on March 17-18, and the overlapping pressures are increasing the vulnerability of the cryptocurrency market.

Chain Reaction of the Five Major Private Credit Funds

(Source: TFTC)

(Source: TFTC)

The wave of private credit withdrawals shows a clear domino effect: when one fund announces restrictions on redemptions, investors rush to withdraw from other funds to prevent them from also closing, further amplifying overall liquidity pressure.

Cliffwater’s flagship fund, with a scale of $33 billion, set a redemption limit of 7% after investors attempted a record 14% quarterly redemption, and only about half of the requests were actually paid out. Morgan Stanley’s North Haven Private Income Fund set a 5% redemption cap and returned only about $169 million, roughly 45.8% of investor requests.

The market for Business Development Companies (BDCs) also signals important information: these instruments are currently trading at about 0.73 times their net asset value, the largest discount since 2020, indicating that credit market investors are actively reducing risk exposure.

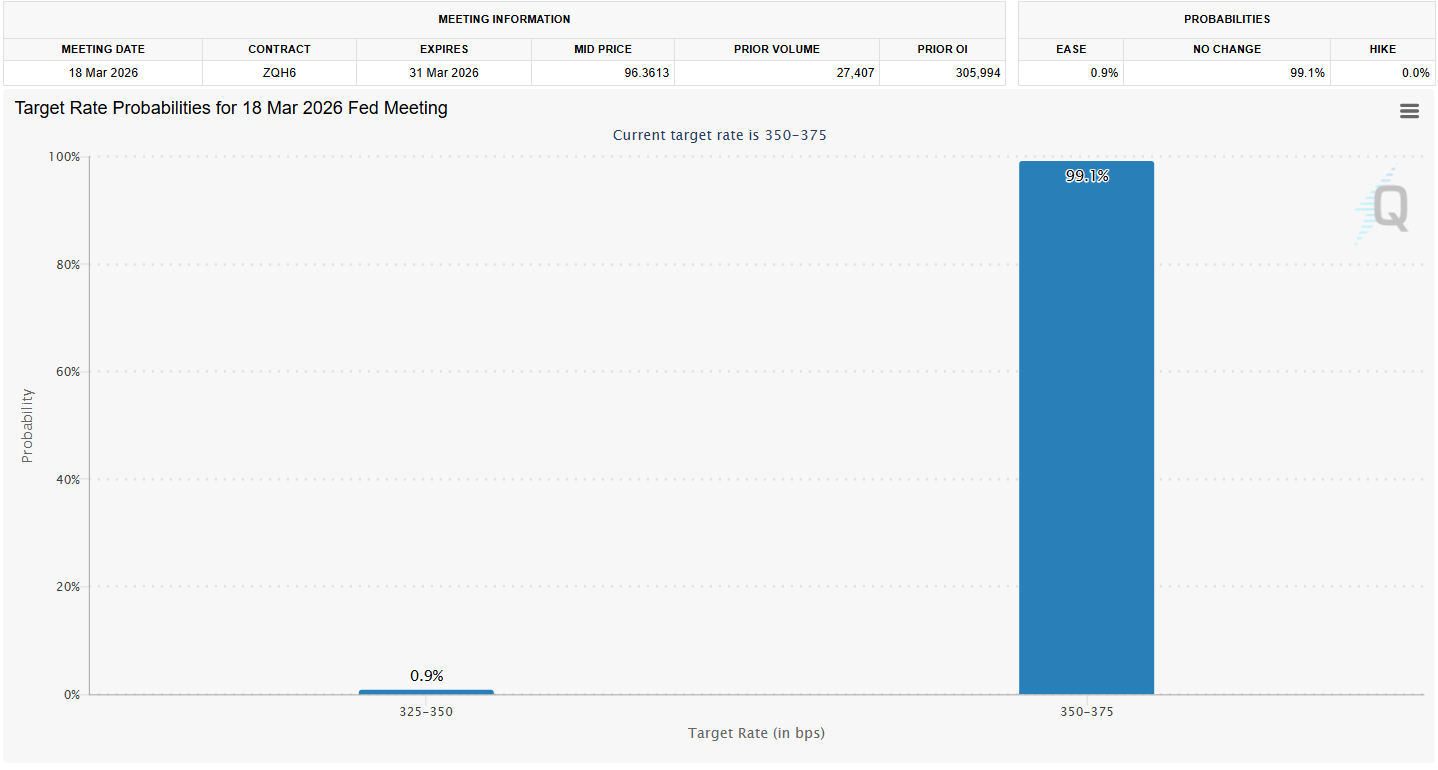

FOMC Timing Overlap: Bitcoin Faces Dual Liquidity Pressures

(Source: CME Fed Watch)

(Source: CME Fed Watch)

The high overlap of timing is a core concern in the current market:

- Historical FOMC patterns: Bitcoin has declined after seven of the eight FOMC meetings in 2025; after the January FOMC kept rates unchanged, Bitcoin dropped from $90,400 to $83,383 within 48 hours.

- Market sentiment: Fear and Greed Index is currently at “Extreme Fear,” marking the most fragile period for the crypto market since 2022.

- Interest rate expectations: CME FedWatch shows over 99% probability of maintaining rates between 3.50% and 3.75%; the rate decision itself has been priced in, with the key variable being Powell’s tone and language.

- Critical support level: If private credit tightening and hawkish statements occur simultaneously, the $62,300 support level will face significant pressure.

Bitcoin remains stable above $71,000, but investors unable to redeem from private credit funds may choose to sell highly liquid assets like Bitcoin and Ethereum to raise cash.

Deutsche Bank AI Credit Exposure and Broad Warnings in Credit Markets

Deutsche Bank disclosed this week that its private credit portfolio has grown to €25.9 billion (about $30 billion), with technology loans surging over one-third to €15.8 billion (about $18.3 billion), heavily concentrated in software companies disrupted by AI. This presents dual risks for the crypto market: traditional software loans face valuation risks from AI competition, and emerging AI infrastructure loans could also form another valuation bubble.

In derivatives markets, the open interest in put options on major US credit ETFs (including HYG, JNK, and LQD) has reached a record 11.5 million contracts, doubling from last year; tech high-yield credit spreads have widened to 556 basis points, 195 basis points above the broad high-yield benchmark, indicating that institutional investors are actively hedging against rising credit risks.

FAQs

Why might private credit fund restrictions lead to Bitcoin sell-offs?

Investors unable to redeem smoothly from private credit funds often need to liquidate highly liquid assets to raise cash. As many institutional allocators hold Bitcoin and Ethereum as their most liquid risk assets, these become the primary sources for raising funds. This indirect “liquidity transmission” can force sell-offs in the crypto market.

Why is the FOMC meeting particularly noteworthy now?

Bitcoin has declined after seven of the eight FOMC meetings in 2025. Coupled with the Fear and Greed Index showing the market at its most fragile since 2022, any hawkish FOMC statement could accelerate the ongoing de-risking in the private credit market. The rate decision itself has been priced in, but Powell’s tone and language are the key variables.

What is the significance of the BDC discount in relation to the private credit crisis?

BDCs are currently trading at 0.73 times their net asset value, the largest discount since 2020, indicating that market funds are actively reducing credit market risk exposure. The BDC discount is often an early indicator of broader credit stress, and together with the shutdown behaviors of the five major private credit funds, forms a composite signal of tightening credit conditions.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.