Market Maker Wintermute reported on Thursday that, for the first time since the start of the four-year halving cycle, Bitcoin has failed to deliver a double price return sufficient to offset the decline in block rewards. Miners’ gross margins have fallen to levels that previously marked the bottom of a bear market. Wintermute believes that the Bitcoin held collectively by miners is a legacy issue from the HODL era, and that “actively managing these assets is the key leverage for miners to gain a structural advantage at the next halving.”

Structural Challenges in Bitcoin Mining: Triple Pressures Evolving Simultaneously

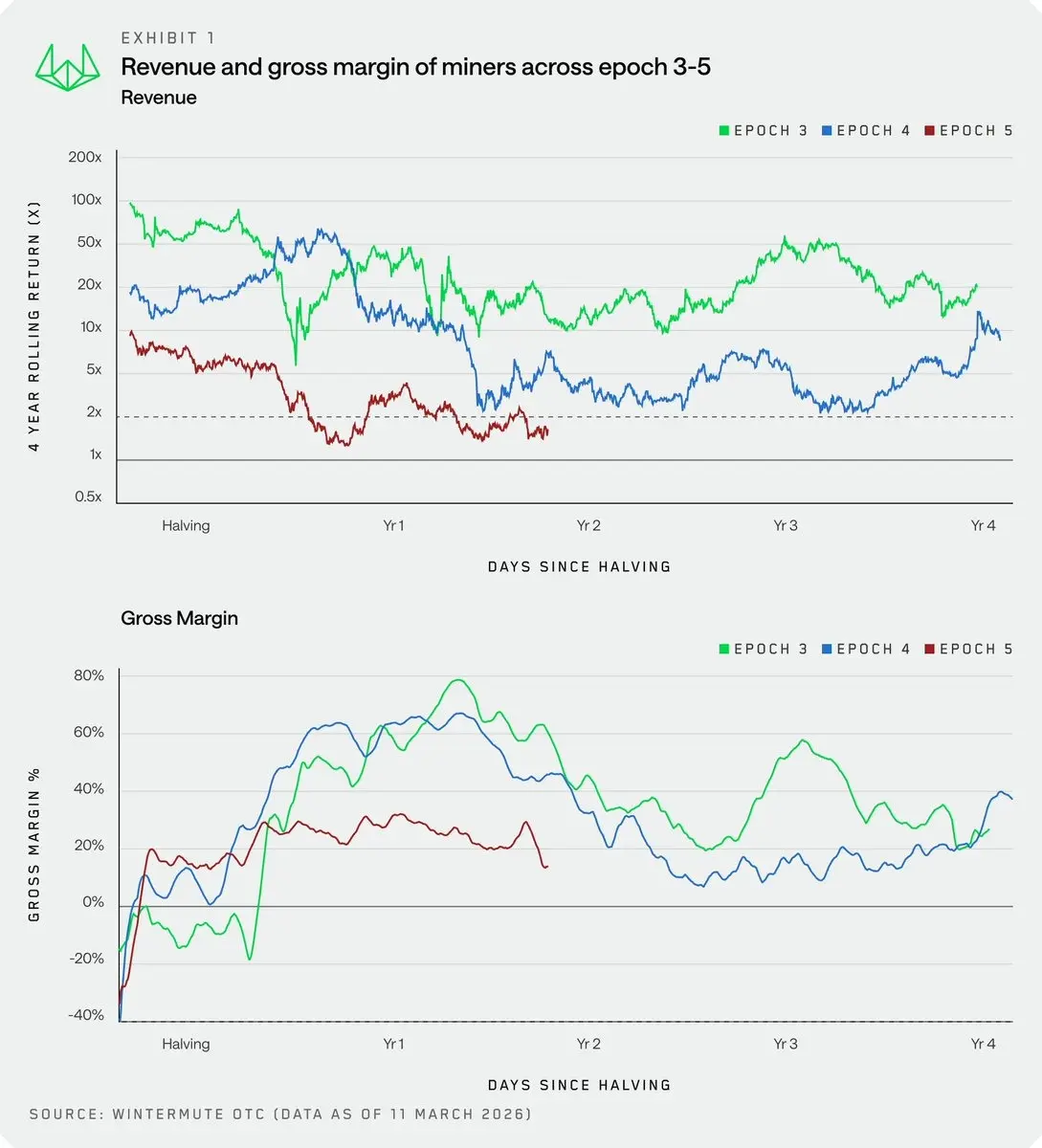

(Source: Wintermute)

Wintermute’s report clearly outlines the current systemic pressures facing the Bitcoin mining industry:

Halving Premium Fails for the First Time in History: In previous four-year market cycles, Bitcoin’s price increases typically enough to compensate for or even surpass the reduction in block rewards caused by halving, allowing miners to remain profitable. However, in this cycle, Bitcoin’s gains have failed to cover the revenue gap created by halving, causing miners’ gross margins to drop to levels previously only seen at bear market lows.

Limited Effectiveness of Transaction Fee Supplement: Besides block rewards, transaction fees have been viewed as a potential supplementary income source. But Wintermute points out that the transaction fee market is “sporadic” rather than structural, making it unsuitable as a stable income buffer.

Energy Costs Continue to Squeeze Profitability: Although miners have built large-scale power infrastructure in low-cost energy markets over the years, energy costs remain a primary pressure on margins, especially in the current profitable environment.

Wintermute characterizes this cycle’s pressures as a “healthy oscillation,” different in nature from the cycles of 2018 and 2022, believing this process aligns with Bitcoin’s design logic and will ultimately make the mining industry “more efficient.”

Wintermute’s Path Forward: From Passive Reserves to Active Asset Management

Wintermute’s core argument is that miners should change their mindset about holding Bitcoin—from “passive reserves” to “operating assets.” Currently, miners collectively hold nearly 1% of the total Bitcoin supply, but “the full suite of capital management tools remains underutilized.”

The report lists two main categories of active management strategies

Active Management: Using derivatives to monetize market risk, including tools like covered calls—selling call options against Bitcoin holdings to collect premiums—and cash-secured puts—setting buy commitments at acceptable prices and collecting option premiums.

Passive Management: Deploy Bitcoin into lending protocols to earn interest, allowing holdings to generate cash flow even during market volatility.

Wintermute explicitly states: “Miners who view Bitcoin holdings as operational assets rather than passive reserves will gain a structural advantage at the next halving.”

AI Transformation: Another Path, but at a High Cost

As Wintermute’s report was released, the industry’s AI transformation wave is accelerating. MARA Holdings filed with the SEC on March 3 indicating plans to sell some Bitcoin to fund AI technology transformation; since October last year, publicly listed miners have sold over 15,000 BTC.

Wintermute acknowledges that the large-scale power infrastructure built in low-cost energy markets is precisely the “most urgently needed and hardest to replicate” core resource for AI data centers. However, the report also clearly states that AI transformation is a “drastic and capital-intensive initiative,” not suitable for all miners, and that Bitcoin mining’s “structurally rigid business model” increases the risks and costs of such a transition.

FAQs

Is there a risk in miners holding Bitcoin and selling covered calls?

The core risk of a covered call strategy is that if Bitcoin’s price surges significantly above the strike price during the option’s life, miners will lose out on upside gains—since they must sell Bitcoin at the preset strike price to the option buyer. In a strong bull market, miners could forfeit substantial potential profits. Therefore, the covered call strategy is more suitable when miners expect limited short-term upside and prefer stable income during sideways or mildly bullish markets.

Why is the failure of the halving premium in this cycle a unique phenomenon in mining history?

In past Bitcoin four-year cycles, post-halving supply reductions usually coincided with demand growth, leading to significant price increases that made miners’ total revenue (hash rate × price) higher after halving than before. In this cycle, although Bitcoin’s price has risen, the increase has not been enough to restore miners’ gross margins to previous cycle levels, creating the first “halving toxicity” in mining history—supply halved but earnings did not proportionally increase.

Is Wintermute’s strategy more suitable for large or small miners?

Active derivatives strategies (covered calls, cash-secured puts) generally require certain technical expertise and market liquidity, making them more suitable for mid-to-large publicly listed miners with substantial Bitcoin holdings. For smaller miners, deploying some Bitcoin into lending protocols for passive income is easier to implement, though it also involves smart contract risks and credit risks associated with lending platforms.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.