Author: Financial Stability Board; Compiler: TaxDAO

This article describes responses to crypto asset risks. It is important to note that this document does not propose new policies, recommendations or expectations for Member State authorities. Instead, it draws on existing policy advice and guidance from the International Monetary Fund (IMF), Financial Stability Board (FSB), international organizations (IOs) and standard-setting bodies (SSBs). Macrofinancial policy, financial regulation, and other policy and regulatory considerations that address legal risk, financial integrity, market integrity, and investor protection are all fundamental elements of an effective policy framework for cryptoassets. The paper concludes by describing additional policy considerations for targeted measures that may be appropriate under certain conditions in jurisdictions with higher macroeconomic risks, such as some emerging market and developing economies.

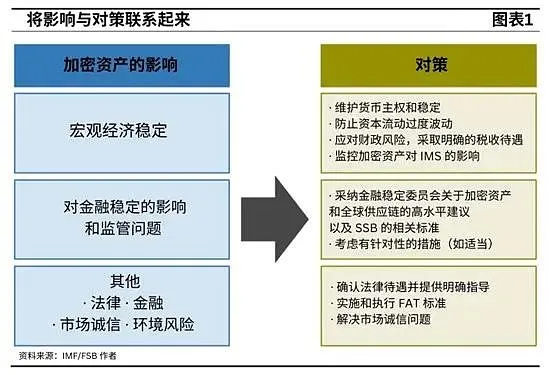

1. Macroeconomic Stabilization Policy

1.1 Maintain currency sovereignty and stability

Developing effective frameworks and policies is the best way to limit crypto-asset substitution. Sound macroeconomic policies and a credible institutional framework are fundamental to protecting monetary sovereignty. A weak monetary policy framework, coupled with fiscal deficits and central bank financing pressures, will undermine currency credibility and encourage currency substitution.

An effective Monetary Policy Framework (MPF) safeguards monetary sovereignty through transparency, coherence and consistency. It includes policy design, implementation, communication and the legal basis for central bank independence. A transparent, coherent and consistent MPF enhances understanding, market expectations and policy effectiveness.

Avoiding large deficits and high debt levels is important to protect monetary sovereignty, especially when the monetary policy framework is weak. Putting pressure on central banks to finance deficits rather than tighten policy could lead to inflationary consequences and increase pressure for currency substitution, which in turn would encourage the use of cryptoassets as a means of payment.

To protect monetary stability, cryptoassets should not be granted official currency or legal tender status. Official means of payment shall be limited to public currencies issued by the state. Cryptoassets carry fundamental risks and should not be considered “money” because they do not meet the three basic conditions of “money” (unit of account, means of exchange, and store of value). Central banks should also avoid holding crypto assets in their official reserve assets due to risks and concerns about the destabilizing effects of the International Monetary System (IMS).

In the case of official use of crypto-assets, governments should minimize fiscal and operational risks. Official payment use should be restricted to avoid government revenue being affected by changes in crypto asset prices. Convertibility guarantees should be avoided to prevent the Treasury from accumulating contingent liabilities, and risks in fiscal management operations should be managed through safeguards and controls.

1.2 Prevent excessive fluctuations in capital flows

Policymakers should take steps to counteract the impact that the adoption of crypto-assets may have on capital flow management measures.

measures, CFM). Possible policy measures include clarifying the legal status of crypto-assets where necessary and ensuring that CFM laws cover crypto-assets and are effectively enforced. Addressing data gaps and leveraging technology can help authorities monitor risks and implement CFM more effectively.

If the effectiveness of CFM mechanisms is reduced due to the adoption of crypto-assets, jurisdictions may need to consider increasing exchange rate flexibility and balancing the competing goals of monetary autonomy, exchange rate stability and financial openness. Given the benefits of international reserves as a buffer against balance of payments crises, managing the risk of increased capital outflows may involve adjustments to international reserves. In such circumstances, macroeconomic policy adjustments may be necessary, such as monetary tightening, macroprudential or fiscal policy.

1.3 Address fiscal risks and adopt clear tax treatments

Fiscal risks arising from widespread adoption of cryptoassets, including those arising from conferring fiat or official currency status, should be identified, analyzed and disclosed. Fiscal risks to governments related to cryptoassets should be promptly assessed, quantified (to the extent possible) and monitored. The widespread use of cryptoassets in weakly regulated environments increases the explicit and implicit fiscal risks governments face from the financial sector.

Identifying and monitoring risks associated with crypto-assets can improve governments’ ability to mitigate and respond to risks, promoting fiscal credibility and the sustainability of public finances. These public finance risks should be included in the government’s fiscal risk statements to improve fiscal transparency.

Tax policies should ensure clear tax treatment of crypto-assets, and tax administration departments should strengthen compliance efforts. Legal provisions should clearly reflect policy decisions regarding the tax treatment of cryptoassets, including income tax/wealth tax and value-added tax, as discussed in detail by Bell et al. Tax authorities should leverage third-party information, especially when it comes to crypto-asset trading platforms, brokers, and other intermediaries, to enhance tax compliance.

Cross-border information sharing and financial regulatory cooperation are critical for effective tax compliance. Adopting a framework such as the Crypto-Asset Reporting Framework (CARF) proposed by the OECD could be beneficial. Improving institutional capabilities, investing in specialized data infrastructure and analytics, and prioritizing the training of tax administrators will be critical to supporting risk analysis and tax audits related to cryptoasset businesses.

1.4 Monitoring the Impact of Crypto-Assets on the International Monetary System (IMS)

The international monetary system may face new challenges, such as more fragmented, large and unstable capital flows, as well as new risks to financial stability and integrity. Crypto-assets may amplify existing vulnerabilities and pose new risks to global financial stability and the international monetary system on multiple fronts.

As stipulated in its Articles of Agreement, the IMF’s primary role is to ensure the stability and efficiency of the international monitoring system. The IMF actively cooperates with member countries through multilateral and bilateral surveillance, capacity development, and lending. When it comes to crypto-assets, an important part of the IMF’s work is to assess macro-financial risks and spillover risks.

Ongoing analysis, rule review and monitoring are imperative. Areas requiring close and ongoing monitoring include (i) the impact of crypto-assets on gross and net cross-border capital flows; (ii) changes in financial intermediation, currency substitution and international currency use; (iii) effects on exchange rates and capital account systems and Impact of CMF; (iv) financial integrity risks; (v) demand and supply of global financial safety net resources. Close monitoring will help inform appropriate regulation and cross-border cooperation between policymakers and international standard-setting bodies.

2. Financial Stability Regulation

2.1. Financial Stability Board’s Global Framework for Cryptoasset Activities

The FSB recommendations provide a global framework for effective regulation and oversight of crypto-asset activities and markets, as well as global stablecoin arrangements. The framework is based on the principle of “same activity, same risk, same regulation” and provides a solid basis for ensuring that crypto asset activities and stablecoins are subject to consistent and comprehensive regulation commensurate with the risks they pose.

The Financial Stability Board framework includes two distinct sets of recommendations. Advice on cryptoassets and markets applies to any type of cryptoasset activity, including stablecoins and activity via DeFi. However, those stablecoins that are widely used as a means of payment and/or store of value across multiple jurisdictions—global stablecoins, GSCs—may pose particular risks to financial stability. As a result, separate supplementary advice has been issued for crypto-asset activities that fall within the GSC’s definition to reflect their particular risks and heightened regulatory and supervisory requirements.

The Financial Stability Board’s recommendations are high-level. The recommendations provide jurisdictional authorities with sufficient flexibility to implement them and adapt to rapidly changing circumstances by applying relevant existing regulations or developing new domestic regulatory frameworks. This approach also leaves ample room for SSBs to develop additional guidance within their respective areas of responsibility to address sectoral issues.

2.2 Financial Stability Board high-level recommendations on cryptoassets

Relevant authorities should have appropriate regulatory powers and should apply comprehensive and effective regulation, supervision, and supervision.

and oversight) requirements. Authorities should possess and utilize necessary or appropriate powers, tools and sufficient resources to regulate, supervise and monitor crypto asset activities and markets, and effectively enforce relevant laws and regulations. The application of these powers and tools should be proportionate to the risks posed and consistent with international standards and the respective mandates of the authorities.

To promote efficient and effective communication, information sharing and consultation, authorities should cooperate and coordinate with each other domestically and internationally. Cooperation and coordination should support different agencies in fulfilling their respective tasks and should encourage consistency in regulatory and supervisory outcomes.

Cryptoasset issuers and service providers should establish comprehensive governance frameworks. This includes establishing clear and direct responsibility and accountability for all functions and activities being carried out.

An effective risk management framework should be established to comprehensively address all significant risks associated with the functions being performed and activities undertaken. This should include addressing risks from operational resilience, cybersecurity safeguards and anti-money laundering/combating the financing of terrorism measures, as well as “appropriate” requirements.

Robust data frameworks are needed to ensure appropriate regulation, supervision and inspection. The data framework should include systems and procedures for collecting, storing, protecting, and reporting data promptly and accurately. Authorities should be able to obtain data at their discretion.

Comprehensive, clear and transparent information about crypto asset markets and services should be provided to users and relevant stakeholders. This information should cover management framework, operations, risk profile and financial position,

Authorities should identify and monitor relevant interconnections within the crypto-asset ecosystem and between the crypto-asset ecosystem and the broader financial system, and address financial stability risks.

Where permitted, cryptoasset service providers that combine multiple functions and activities should be subject to appropriate regulation, supervision and inspection. This should comprehensively address risks associated with individual functions and risks arising from combinations of functions, including conflicts of interest and the segregation of certain functions. In some jurisdictions, this combination is not allowed, in which case authorities should take strong measures such as the legal disaggregation and separation of certain functions.

2.3 Financial Stability Board’s high-level recommendations on global stablecoins

The Financial Stability Board’s high-level recommendations take a broad approach to global stablecoins (GSCs). International standards designed for specific sectors focus on unique functions within the purview of the relevant standards-setting body. When international sectoral standards are applied to global stablecoins for a specific economic function, these standards will address risks specific to that economic function and, therefore, relevant authorities should enforce these international standards.

The Financial Stability Board’s GSC advice complements other crypto-asset advice and reflects the GSC’s special risks and heightened regulatory and supervisory requirements. The relevant authorities should use appropriate regulatory powers to provide comprehensive oversight of the GSC’s activities and functions. These recommendations promote cross-border cooperation and information sharing, sound data frameworks and effective risk management frameworks arranged by the GSC. These recommendations include additional requirements to address the specific risks of GSCs.

GSC arrangements should have appropriate recovery and resolution plans in place. The relevant authorities should require the GSC to arrange for the development of appropriate plans to support recovery, dissolution or orderly winding up under the applicable legal (or insolvency) framework.

GSC issuers and, where applicable, other participants in GSC arrangements, should provide all users and relevant stakeholders with comprehensive and transparent information about the operation of the GSC arrangements. This information should include the governance framework, any conflicts of interest and their management, redemption rights, stabilization mechanisms, operations, risk management framework and financial position.

GSC arrangements should be subject to strict call rights, stabilization and prudential requirements to maintain a stable value at all times and reduce the risk of runs. Authorities should require GSCs to arrange to provide all users with robust legal claims against the issuer and/or underlying reserve assets, with guaranteed timely redemptions. For GSCs denominated in a single fiat currency, redemptions shall be made at face value into that fiat currency.

3. Other policies and regulations

3.1 Legal considerations

In some jurisdictions, it may be necessary to clarify the application of existing laws or to assess whether new laws are needed. In the absence of such legal certainty, jurisdictions should consider three actions, which are not mutually exclusive, may involve legal reform and should be developed with the participation of the private sector and based on guidance from international organizations:

· Modernize private law through targeted legislative reform where necessary. In some jurisdictions, private law may need to be modernized to clarify the classification of cryptoassets and the rules for their trading. Where there are gaps in the existing framework, legislative reforms could focus on areas where there is friction between private law and new technologies, such as in Switzerland, Liechtenstein and Germany, to avoid delays and inconsistencies with the wider legal framework.

·When necessary, clarify the application of financial laws and the treatment of crypto assets. This can be achieved through various methods. When crypto-asset activities fall within established legal categories, existing legal and regulatory frameworks can be enforced (for example, the application of securities laws to crypto-assets). If gaps exist and existing frameworks are not yet applicable, jurisdictions could amend existing laws to explicitly cover specific activities related to crypto-assets (such as Japan), or issue bespoke laws on crypto-assets (such as the European Union’s Crypto-Asset Markets Regulation 》) or laws regarding financial technology (“fintech”), of which cryptoasset activities are a subset (as in Mexico).

·Reduce the issue of under-taxation of transactions involving crypto-assets. This requires a transparent and predictable tax framework, coupled with international cooperation. While tax laws generally apply to crypto-assets based on their legal characteristics, adjustments may be needed to provide clarity and certainty and to achieve a country’s specific policy objectives. Tax administrations should provide timely and comprehensive guidance to taxpayers, complementing existing frameworks to increase transparency and predictability of treatment. In addition, countries should clarify payment and reporting obligations, including those of cryptoasset service providers.

3.2 Financial Integrity Supervision

Jurisdictions should implement FATF standards in the area of virtual assets to protect their financial systems and the global economy from the threats of money laundering, terrorism financing and the proliferation of weapons of mass destruction. According to the FATF standards on virtual asset service providers adopted in 2019, jurisdictions should assess the money laundering and terrorism financing risks associated with virtual asset activities and take appropriate measures to reduce these risks; issue licenses to virtual asset service providers or be registered; and supervise the sector in the same manner as other financial institutions. At the same time, virtual asset service providers should be required to implement risk mitigation measures, including customer due diligence, record keeping and reporting of suspicious transactions, and the imposition of targeted financial sanctions. Virtual asset service providers should be required to apply the “Travel Rule” on payment transparency and obtain, hold and securely transmit originator and beneficiary information when making transfers. The FATF adopted revised guidance on a risk-based approach to virtual assets in 2021 to help jurisdictions and virtual value-added service providers understand their AML/CFT obligations and effectively implement the FATF’s work group standards.

The borderless nature of the cryptoasset ecosystem limits the effectiveness of regulation by individual countries. Given that a particular VAS provider may be subject to multiple jurisdictions’ AML/CFT frameworks, cooperation and information sharing between jurisdictions is essential to improve understanding of crypto-asset-related issues at global and jurisdictional levels. Awareness of money laundering/terrorism financing risks is critical. Inconsistent enforcement of FATF standards also creates opportunities for regulatory arbitrage. Collective action and widespread implementation of a FATF-compliant AML/CFT framework are therefore critical to reducing illicit financial risks in the crypto-asset space. Recognizing the urgent need to address these geographical disparities, the FATF adopted a roadmap in February 2023 to accelerate the global implementation of AML/CFT controls and oversight in the crypto-asset sector.

Financial integrity is one of the key objectives of an effective policy framework. Jurisdictions should consistently implement FATF standards and engage in effective international cooperation. The IMF should continue its efforts to advise members on financial integrity issues related to crypto-assets in its surveillance, lending and assessment work, and support its members in implementing effective AML/CFT frameworks through its capacity-building activities .

3.3. Market Integrity Supervision

Jurisdictions should implement and apply the IOSCO Principles and Standards to economically equivalent crypto assets and activities to address the substantial and proximate market integrity and investor protection risks in the industry, including interests conflicts, customer asset protection, market manipulation, operational risk, retail access suitability and cross-border issues.

3.4 Other targeted measures

In addition to implementing policy recommendations and standards from the International Monetary Fund, Financial Stability Board, Financial Action Task Force and SSB, some authorities may consider imposing targeted or time-bound broad restrictions to manage risks from crypto-assets . A blanket ban that would make all crypto-asset activities, such as trading and mining, illegal could be costly and technically demanding to enforce. Due to the inherently borderless nature of crypto-assets, these bans also tend to increase incentives for circumvention, leading to increased potential financial integrity risks and possible inefficiencies. A ban in one jurisdiction may also result in activities being moved to other jurisdictions, creating spillover risks. The decision to ban is not a “simple choice” and should be informed by an assessment of money laundering and terrorism financing (ML/TF) risks as well as other considerations, such as significant capital outflows and other public policy objectives.

Targeted restrictions are justified in some circumstances to manage specific risks or to support the regulatory framework for authorities with limited resources. For example, targeted restrictions may be useful when countries experience significant capital outflows, severe currency substitution, unacceptable levels of money laundering/terrorist financing risks, and/or risks to consumers and markets. These restrictions may be specific to certain products (e.g. privacy coins), activities (e.g. payments in Ukraine, financial promotions in Singapore, Spain, UK) or entities (e.g. banks in Nigeria). Targeted restrictions may be needed in the short term while countries improve their internal capabilities, including knowledge and awareness, to respond to regulation.

Even if jurisdictions consider imposing restrictions on a temporary basis, such restrictions should be viewed as part of a larger policy response. Restrictive measures should not replace sound macroeconomic policies, credible institutional frameworks, and comprehensive regulation and supervision, which are the first line of defense against the macroeconomic and financial risks posed by crypto-assets.