Author: Jasper De Maere

Compiled by: Deep Tide TechFlow

Preface

Liquidity drives the cryptocurrency cycle, but inflows through stablecoins, ETFs, and DATs (Digital Asset Trusts) have noticeably slowed.

Global liquidity remains strong, but higher SOFR (Secured Overnight Financing Rate) is directing funds into government bonds rather than the crypto market.

Currently, cryptocurrencies are in a self-financing phase, with capital cycling internally, waiting for new inflows to return.

Liquidity determines every crypto cycle. While long-term technological applications may be the core driver of the crypto story, it is the movement of funds that truly influences price changes. Over the past few months, the momentum of capital inflows has weakened. In the three main channels through which capital enters the crypto ecosystem—stablecoins, ETFs, and Digital Asset Trusts (DATs)—the flow momentum is diminishing, causing cryptocurrencies to be in a self-financing rather than expansion phase.

Although technological adoption is an important driver, liquidity is the key factor that drives and defines each crypto cycle. It’s not just about market depth but also about the availability of funds themselves. When global money supply expands or real interest rates decline, excess liquidity inevitably seeks risk assets. Historically, especially during the 2021 cycle, cryptocurrencies have been among the biggest beneficiaries.

In previous cycles, liquidity primarily entered the digital asset space through stablecoins, which serve as the core fiat on-ramp. As the industry matures, three major liquidity channels are becoming critical in determining new capital inflows into crypto:

- Digital Asset Trusts (DATs): Tokenized funds and yield structures connecting traditional assets with on-chain liquidity.

- Stablecoins: On-chain representations of fiat liquidity, providing collateral for leverage and trading activities.

- ETFs: Entry points for passive investment and institutional capital exposure to BTC and ETH in traditional finance.

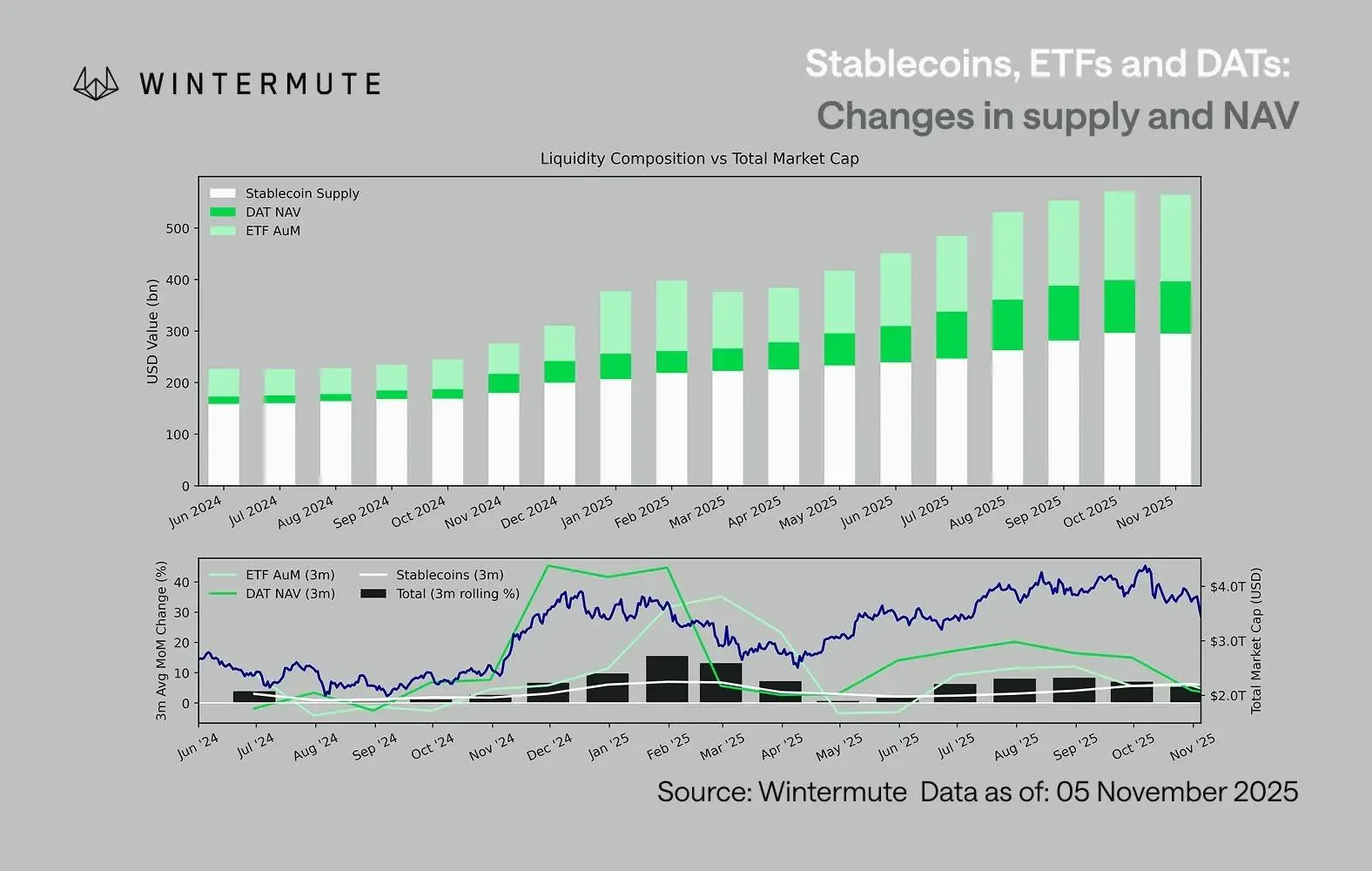

By combining ETF Assets Under Management (AUM), DAT Net Asset Value (NAV), and the number of issued stablecoins, it’s possible to reasonably estimate the total capital flowing into digital assets. The chart below shows the trend of these components over the past 18 months. At the bottom, it’s clear that total volume correlates closely with the overall market cap of digital assets; when inflows accelerate, prices tend to rise.

A key observation is that the inflows into DATs and ETFs have significantly slowed. Both performed strongly in Q4 2024 and Q1 2025, with a brief rebound in early summer, but this momentum has since waned. Liquidity (M2 money supply) is no longer flowing into the crypto ecosystem as naturally as at the start of the year. Since early 2024, the total size of DATs and ETFs has grown from approximately $40 billion to $270 billion, while stablecoin volume has doubled from about $140 billion to roughly $290 billion. Although this indicates strong structural growth, it also shows a clear slowdown.

This deceleration is crucial because each channel reflects different sources of liquidity. Stablecoins represent risk appetite within the crypto industry, DATs capture institutional demand for yields, and ETFs reflect broader traditional financial (TradFi) allocation trends. The simultaneous slowdown across all three suggests a general reduction in new capital deployment, not just a rotation between products. Liquidity isn’t disappearing; it’s merely cycling within the system rather than expanding.

From the broader economy outside crypto, liquidity (M2 money supply) is also not stagnant. Although higher SOFR rates have temporarily constrained liquidity, making cash yields attractive and locking funds into government bonds, the global cycle remains accommodative. The US’s quantitative tightening (QT) has officially ended. The overall structural environment remains supportive; currently, liquidity is being allocated to other risk assets, such as equities.

As external inflows decrease, market dynamics become more insular. Capital is shifting more between mainstream coins and altcoins rather than new net inflows, creating a “player versus player” (PVP) scenario. This explains why market rebounds tend to be short-lived and why market breadth narrows, even as total assets under management (AUM) remain stable. The recent volatility peaks are mainly driven by liquidation cascades rather than sustained trend formation.

Looking ahead, any significant revival in one of the liquidity channels—such as renewed stablecoin issuance, new ETF launches, or increased DAT issuance—would signal macro liquidity flowing back into digital assets. Until then, cryptocurrencies remain in a self-financing phase, with capital cycling internally without generating value expansion.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

NYSE Lifts Crypto Options Cap Across 11 BTC and ETH ETFs

Two NYSE-affiliated venues have scrapped the 25,000-contract cap on options tied to 11 crypto ETF options, a move the exchanges filed with the Federal Register on March 10. The Securities and Exchange Commission acknowledged the rule alterations on Sunday by waiving the standard 30-day waiting

CryptoBreaking36m ago

NYSE Exchanges Remove 25,000-Contract Options Cap on 11 Bitcoin and Ether ETFs

NYSE Arca and NYSE American have removed the 25,000-contract position and exercise limits on options tied to 11 spot Bitcoin and Ether exchange-traded funds (ETFs), with the rule changes filed on March 10, 2026, becoming immediately effective after the Securities and Exchange Commission (SEC) waived the standard 30-day waiting period.

CryptopulseElite50m ago

Gate Daily Report (March 23): MicroStrategy Releases Bitcoin Buy Signal; MajiDaBro's ETH Liquidation Incurs Losses of 30.35 Million

Bitcoin has continued to decline to around $67,950, with MicroStrategy founder Michael Saylor reiterating a buy-the-dip strategy. Huang Licheng's highly leveraged ETH position was completely liquidated, with losses exceeding $30.35 million. Fidelity has called on the US SEC to improve its regulatory framework for crypto assets. US stocks have broadly declined, and market sentiment remains cautious.

MarketWhisper53m ago

Bitcoin Miners' Mining Cost Reaches $88,000, Market Price $69,200, Average Loss of 21%

Bitcoin miners currently have an average production cost of $88,000, with market prices around $69,200, resulting in losses of 21%. Mining difficulty has decreased by 7.76%, with hash price approaching the break-even line. Most mining enterprises are shifting toward AI business, and increased miner Bitcoin sales are adding selling pressure to the market. The next difficulty adjustment is expected in early April, and if conditions persist, further downward adjustments may occur.

GateNews54m ago

Tianqiao Capital Founder: BTC Four-Year Cycle Still Valid, Expects Rally to Resume in 2026 Q4

Skybridge Capital founder Anthony Scaramucci stated that Bitcoin's current bear market can be explained by the four-year cycle theory, with long-term holders concentrating their selling around $100,000. He predicts that Bitcoin will rebound in the fourth quarter of 2026, marking the start of a new bull market cycle. While institutional investor inflows and ETF capital flows have suppressed the four-year cycle, they have not completely eliminated its pattern.

GateNews1h ago